Introduction to M&A

What it is

Mergers & Acquisitions (M&A) is the umbrella term for transactions in which companies combine or one acquires another to create value. In practice, “mergers” are relatively rare; most real-world deals are acquisitions (friendly or hostile) that aim to reshape competitive position, accelerate growth, or unlock efficiencies.

Why it matters

M&A is a core IB product because it blends strategy (why do the deal?), finance (how much is it worth and how to pay?), and execution (how to negotiate, diligence, and integrate?). For candidates, fluency in the rationale and process signals you can speak to both CEOs and CFOs.

How M&A creates value (high level)

- Synergies: Cost takeout (overlap reduction, scale) and revenue uplift (cross-sell, new geographies).

- Speed: Faster than building in-house—enter markets, add products, acquire IP/talent.

- Strategic control: Remove competitors (horizontal) or secure the supply chain/distribution (vertical).

- Portfolio shaping: Buy/grow “winners,” divest or carve out non-core assets.

Common integration archetypes

- Horizontal integration: Acquire a competitor to gain share and scale.

- Vertical integration: Buy a supplier or customer to improve margins and reliability.

- Capability acquisition: Buy tech, talent, or brands to enhance the core.

Interview angle

Be ready to define M&A crisply, distinguish merger vs. acquisition, and give two or three value creation levers with a quick example each (e.g., “horizontal = remove competition; vertical = supply chain efficiency; capability = IP/talent”).

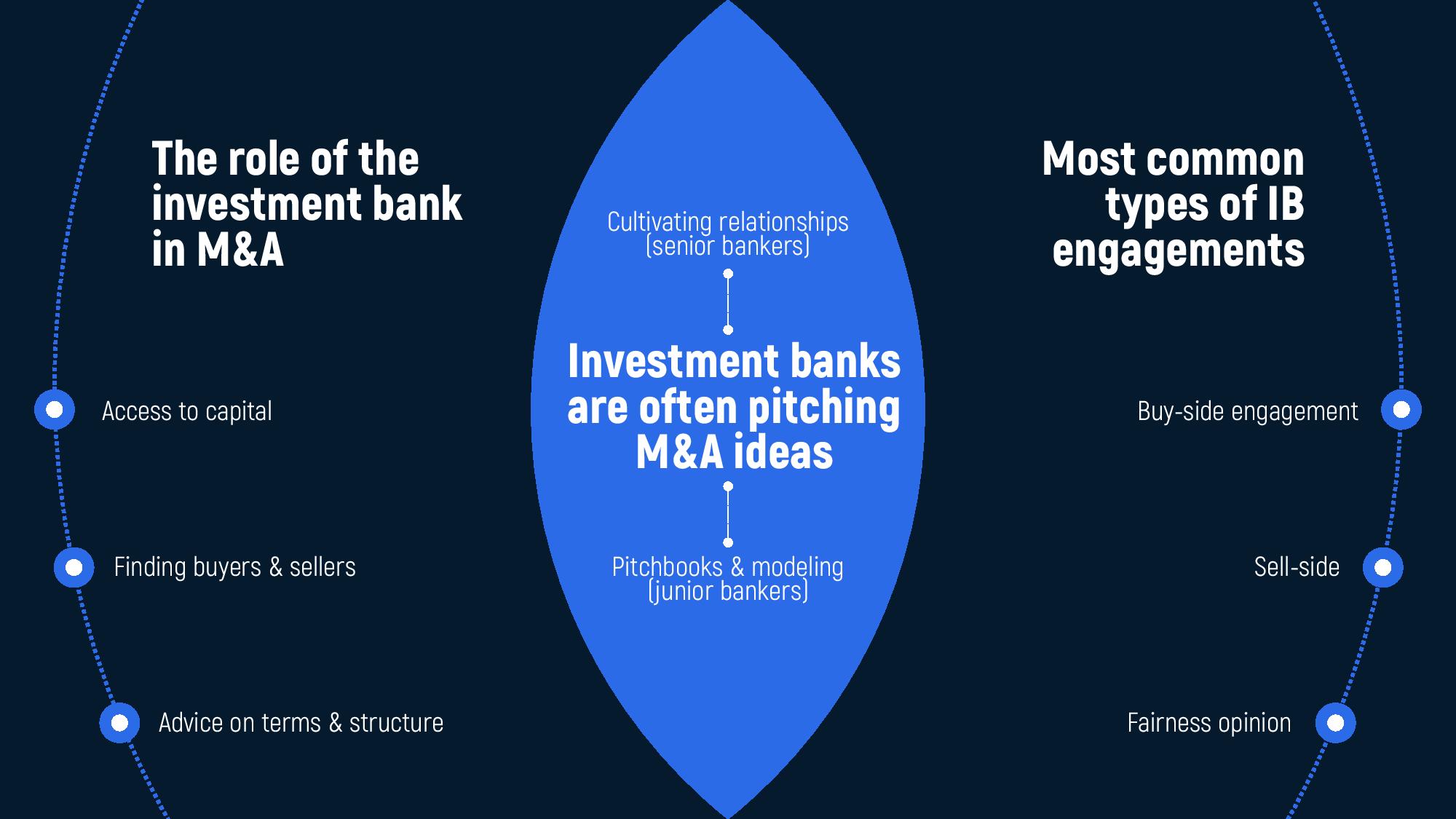

The role of investment banks in M&A

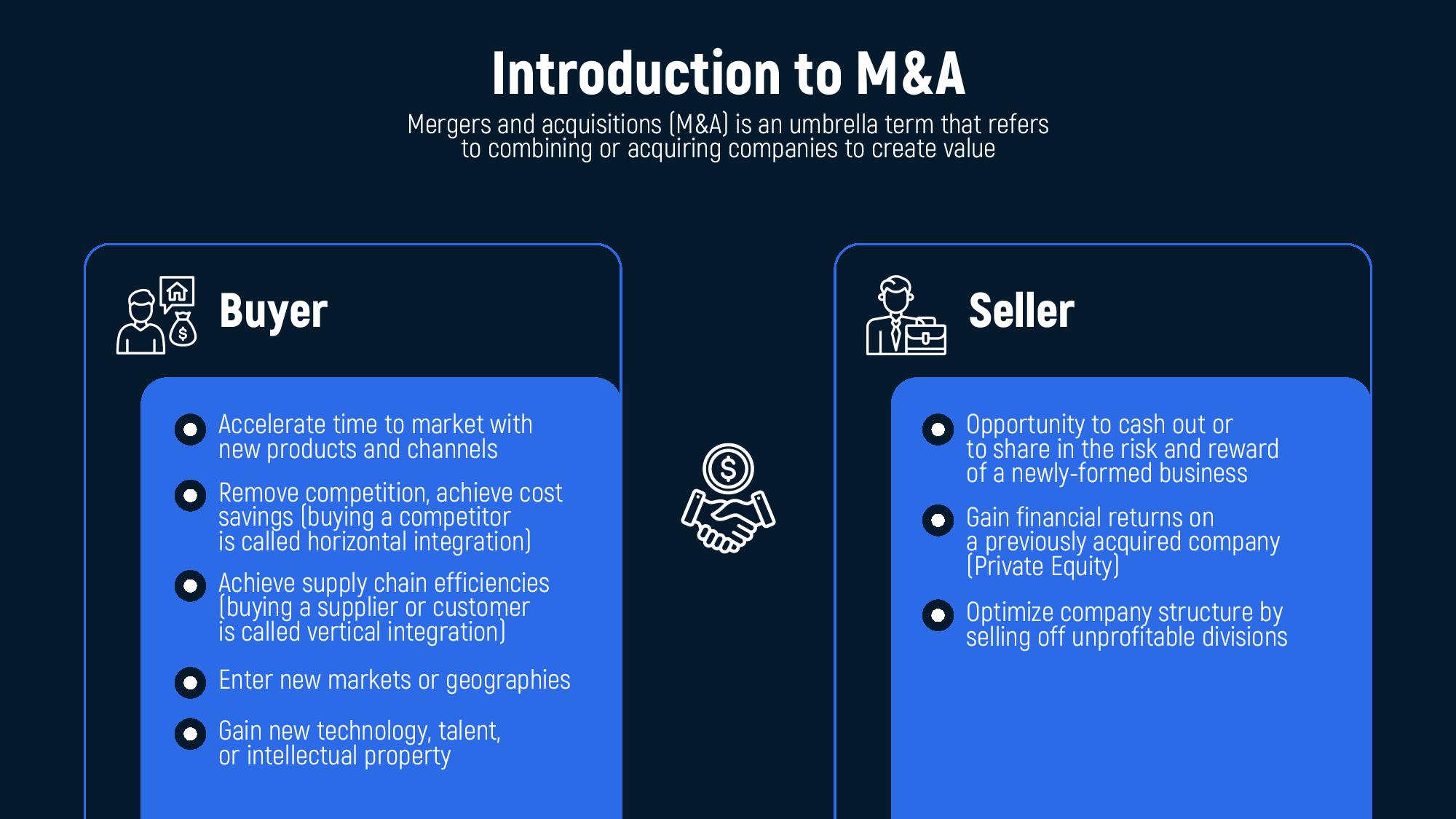

Buyer motivations (what they’re solving for)

- Accelerate time-to-market: Acquire products, channels, or tech to move faster than organic build.

- Remove competition / gain share: Classic horizontal rationale to consolidate fragmented markets.

- Supply-chain efficiencies: Vertical plays (supplier/customer) to reduce cost/volatility and improve margins.

- Enter new markets/geographies: Buy a foothold with local brand, licenses, and distribution.

- Acquire IP/talent/data: Defensive or offensive capability building (e.g., AI labs, patents, niche teams).

Seller motivations (why sell now)

- Liquidity / partial cash-out: Founders or sponsors crystallize value; de-risk while keeping some upside.

- Sponsor exits: Private equity realizing returns on a prior acquisition (full or secondary sale).

- Portfolio optimization: Divest underperforming or non-core divisions (focus capital on core growth).

- Partner to scale: Combine with a larger platform to access capital, customers, or operational excellence.

What IB interviewers listen for

- You tie each motive to measurable outcomes (e.g., cost per unit, margin uplift, market share).

- You can classify motives as horizontal/vertical/capability and discuss integration complexity.

- You note that some motives raise risk (overpaying for synergies, culture clash, regulatory scrutiny).

Mini checklists to sound polished

- For buyers: “What’s the synergy model? Timing, cost to achieve, one-offs vs. run-rate, and risks?”

- For sellers: “What’s the narrative to buyers? Clean financials, credible growth plan, clear carve-out perimeter?”

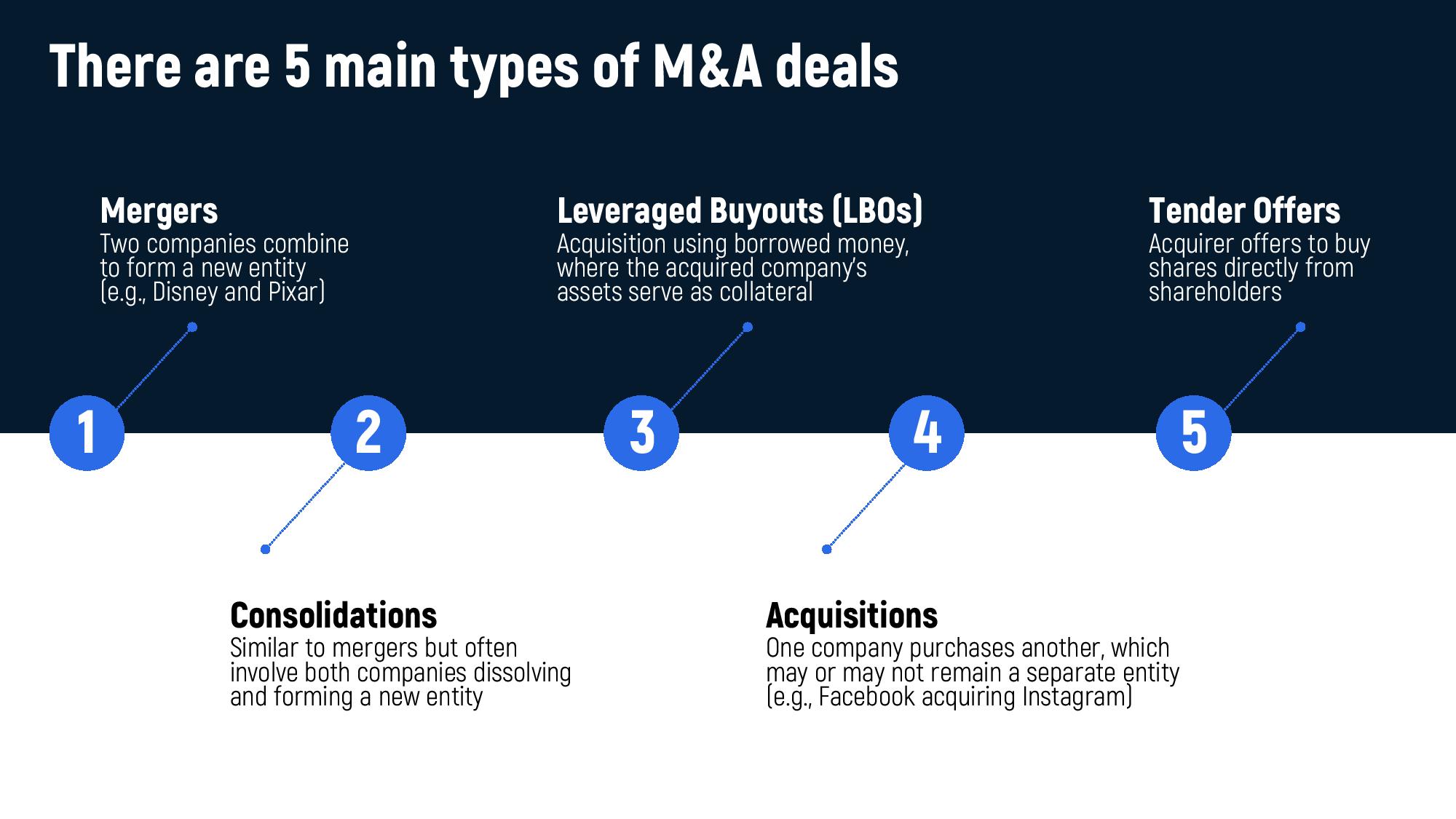

Types of M&A deals

Mergers

A merger occurs when two companies of roughly equal size agree to combine into a single entity. In reality, these are rare because it’s difficult to find two firms willing to give up independence equally. True mergers often happen in stock-for-stock transactions, branded as “mergers of equals.”

Interview insight: Be prepared to note that many “mergers” are actually acquisitions marketed as mergers to make the deal more palatable.

Acquisitions

An acquisition happens when one company (the acquirer) buys another (the target), either through cash, stock, or a mix. These are the most common form of M&A.

- Friendly acquisition: The target’s management and board agree to the deal.

- Hostile acquisition: The buyer bypasses management, appealing directly to shareholders (via tender offer or proxy fight).

Interview insight: You may be asked: “What’s the difference between a friendly and hostile takeover?” Keep the explanation short and crisp.

Consolidations

In a consolidation, two or more companies combine to form a completely new entity, and the old companies cease to exist. It’s less common but can be seen in industries with heavy regulation or need for scale (e.g., banking consolidations).

Tender offers

A tender offer is when a buyer goes directly to the shareholders of a company, offering to purchase shares at a premium to gain control. Tender offers are often associated with hostile takeovers but can be friendly as well.

Leveraged Buyouts (LBOs)

In an LBO, a financial buyer (often private equity) acquires a company using a significant portion of borrowed funds, secured by the target’s assets and cash flows. The goal is to generate strong equity returns by paying down debt and improving operations.

Interview insight: A common IB interview question is: “What is an LBO and why does it work?” A concise answer is: “It’s the acquisition of a company financed largely with debt, relying on cash flows and asset sales to repay debt and deliver equity returns.”

Key takeaway for interviews

When asked about deal types, don’t just list them. Link each to a real-world context:

- Merger of equals: Daimler–Chrysler.

- Acquisition: Facebook buying Instagram.

- Tender offer: Kraft’s acquisition of Cadbury.

- LBO: Blackstone’s buyout of Hilton.

This demonstrates both technical knowledge and commercial awareness.

Are You Ready for a Career a Top Company?

Answer three questions and get a personalized breakdown.

Strategic vs. financial buyers

In M&A, it’s crucial to distinguish between strategic buyers and financial buyers. Both have different goals, approaches, and implications for valuation and deal structure.

Strategic buyers

Who they are: Corporations operating in the same or adjacent industries (e.g., Microsoft buying LinkedIn, Disney buying Pixar).

Motivations:

- Expand market share.

- Enter new geographies or customer segments.

- Acquire complementary products, technology, or talent.

- Realize synergies — cost reduction (shared overhead, supply chain) and revenue growth (cross-selling, bundling).

Key point for interviews: Strategic buyers often justify higher valuations because they can pay for the future synergies they expect to capture.

Financial buyers

Who they are: Investment firms such as private equity funds, hedge funds, or family offices (e.g., Blackstone, KKR).

Motivations:

- Purely financial return (IRR, multiple of invested capital).

- Buy, improve operations, and exit in 3–7 years.

- Often use leverage (debt) to boost equity returns (LBO model).

Key point for interviews: Financial buyers usually pay less than strategic buyers since they can’t realize synergies. Their edge comes from structuring, leverage, and operational improvements.

Why this distinction matters

- Valuation: Strategic buyers = synergy premium; financial buyers = discipline around IRR.

- Negotiations: A seller may prefer strategics for higher price, but financials can offer faster, cleaner deals.

- Exit strategy: Financial buyers look for resale/IPO, while strategics usually hold long term.

Interview question to expect:

- “What’s the difference between a strategic and a financial buyer?”

- “Who can pay more for a company, and why?”

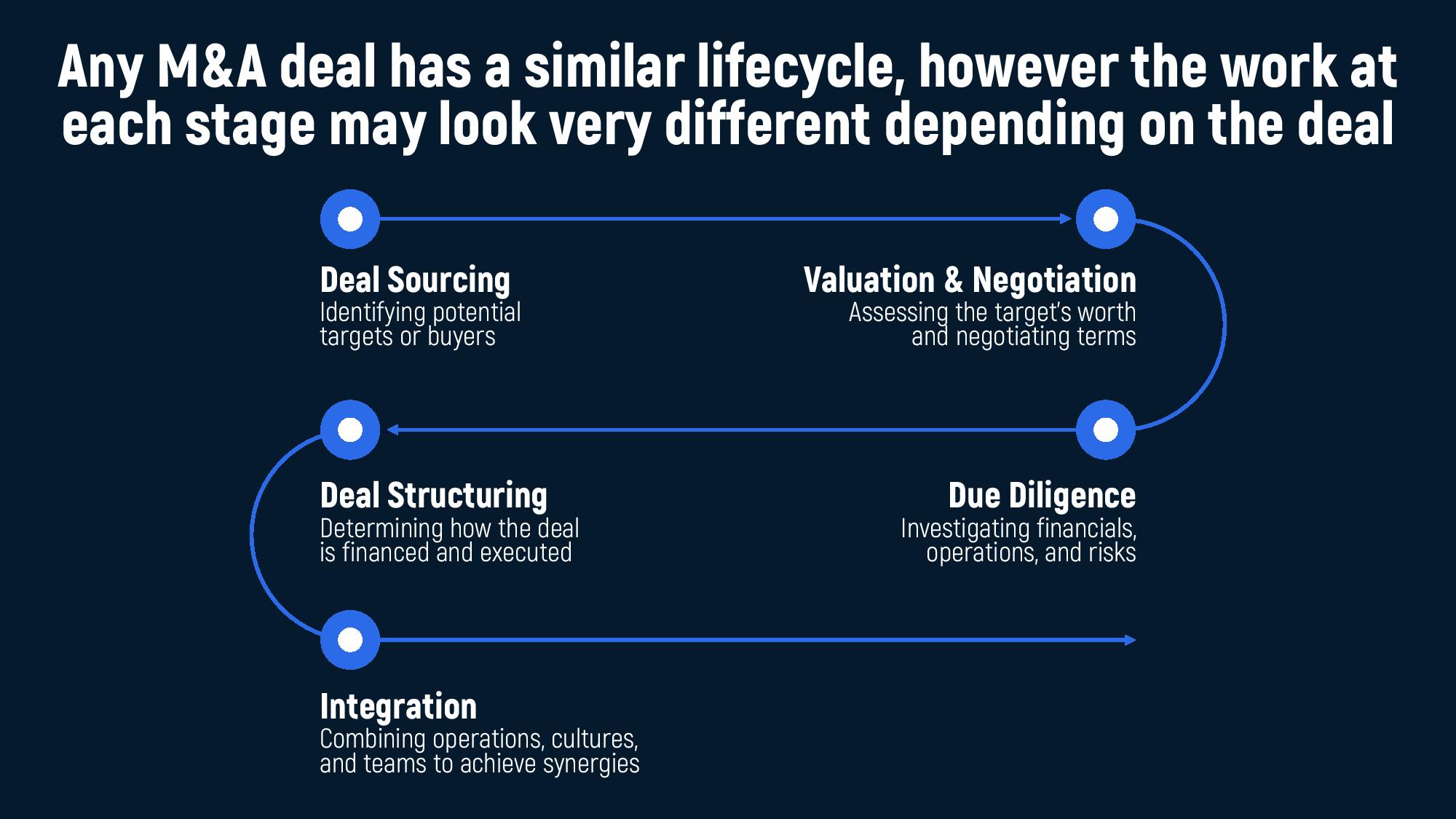

The M&A lifecycle

Every M&A transaction follows a structured process, even though the details vary by industry, geography, and whether it’s a buy-side or sell-side mandate. Understanding the lifecycle of a deal is essential both for bankers executing transactions and for candidates interviewing in IB.

1. Deal sourcing

Identifying potential targets (buy-side) or buyers (sell-side). Investment banks leverage industry knowledge, client relationships, and market screening tools to generate opportunities.

2. Initial valuation & negotiation

Preliminary analysis of the target’s value using methods such as comps, precedent transactions, and DCF. Early discussions with management test alignment on price and structure.

3. Deal structuring

Agreeing on form of consideration (cash, stock, debt, hybrid) and transaction type (merger, acquisition, LBO, tender offer). Structuring also involves planning around tax, regulatory, and financing constraints.

4. Due diligence

A deep dive into the target’s financial, legal, operational, and commercial health. The goal is to validate assumptions, uncover risks, and avoid surprises post-close. For bankers, diligence is about coordinating experts and ensuring data flows smoothly.

5. Closing & integration

Final agreements are signed (Share Purchase Agreement, Merger Agreement, etc.), funds are exchanged, and the new ownership structure takes effect. The hardest part often comes after closing: integration of people, systems, and culture to actually realize synergies.

Interview angle:

A common question is: “Walk me through the steps of an M&A process.”

A strong answer is to briefly list these five steps with one sentence on each — it shows structured knowledge without overloading details.

Key drivers of M&A activity

Behind every transaction lies a strategic or financial rationale. Understanding why companies pursue M&A is crucial, because it determines valuation, deal structure, and integration priorities.

Market share expansion

Companies acquire competitors to strengthen their position, consolidate fragmented industries, or defend against new entrants.

Example: AB InBev’s acquisitions of smaller brewers to dominate global beer markets.

Accelerated growth

M&A is often faster than organic expansion. Instead of spending years building capabilities, firms buy ready-made platforms.

Example: Facebook acquiring Instagram to capture mobile users instantly.

Entry into new markets

Geographic expansion or access to new customer segments can be achieved efficiently via acquisition.

Example: Walmart entering the UK through the acquisition of Asda.

Access to technology, IP, and talent

Acquisitions can deliver proprietary know-how, patents, or niche teams that would be hard to build internally.

Example: Google acquiring DeepMind for AI capabilities.

Synergies (cost and revenue)

Perhaps the most cited driver:

- Cost synergies – economies of scale, overlapping functions, shared infrastructure.

- Revenue synergies – cross-selling, bundling, expanded distribution.

Example: Disney buying Pixar → cross-franchise revenue synergies and shared creative resources.

Financial engineering & tax benefits

Sometimes deals are motivated by balance sheet optimization, access to cash, or tax efficiencies (though regulators scrutinize this closely).

Interview angle:

Expect questions like:

- “Why might a company pursue an acquisition instead of organic growth?”

- “What are synergies, and how do they affect valuation?”

A strong answer highlights strategic rationale + synergies, then gives a real-world example.

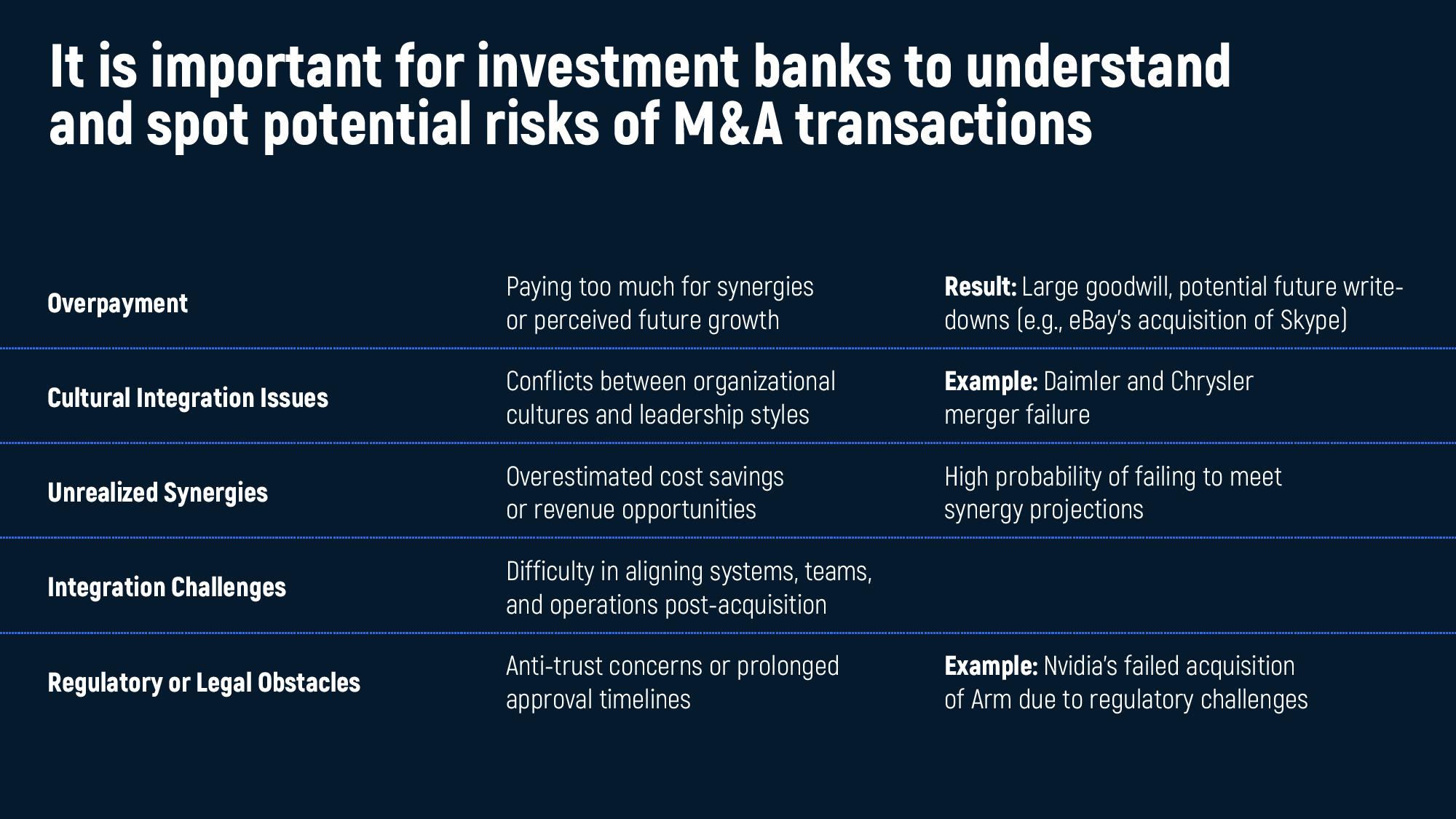

Risks and challenges in M&A

While M&A can unlock growth and value, it also carries significant risks. Many high-profile deals fail to deliver the expected returns, often due to overoptimism or poor execution. For bankers, recognizing these risks is key when advising clients; for candidates, being able to discuss them shows maturity and realism.

Overpayment and goodwill write-downs

In competitive auctions, buyers may overpay, assuming optimistic synergies that never materialize. This often leads to inflated goodwill on the balance sheet and later impairment charges.

Example: HP’s $11B write-down after its Autonomy acquisition.

Unrealized synergies

Capturing cost or revenue synergies is difficult in practice. Integration costs may outweigh savings, or cultural barriers may block cross-selling.

Interview tip: Always stress that synergies are estimates, not guarantees.

Cultural and organizational integration

Merging two organizations often triggers culture clashes, leadership conflicts, and employee turnover. Poor cultural fit can undermine even financially sound deals.

Example: Daimler–Chrysler merger, where cultural misalignment derailed integration.

Regulatory and legal hurdles

Large deals attract scrutiny from antitrust authorities, governments, and regulators. Delays or outright blocks can destroy value or even prevent completion.

Example: U.S. regulators blocking AT&T’s attempted acquisition of T-Mobile in 2011.

Execution complexity

Coordinating diligence, financing, legal agreements, and integration requires precision. Weak execution can derail timelines and add unexpected costs.

Interview angle:

Questions you might face:

- “Why do so many M&A deals fail?”

- “What are the main risks in pursuing an acquisition?”

The best answers list 2–3 risks, illustrate them with a quick example, and emphasize that success depends on integration and realistic valuation.

Real-life examples of M&A successes and failures

One of the best ways to understand M&A is to study real deals. Some transactions become case studies in value creation, while others are remembered as cautionary tales. Interviewers often expect candidates to cite examples — it shows not just theory, but also awareness of business history.

Success stories

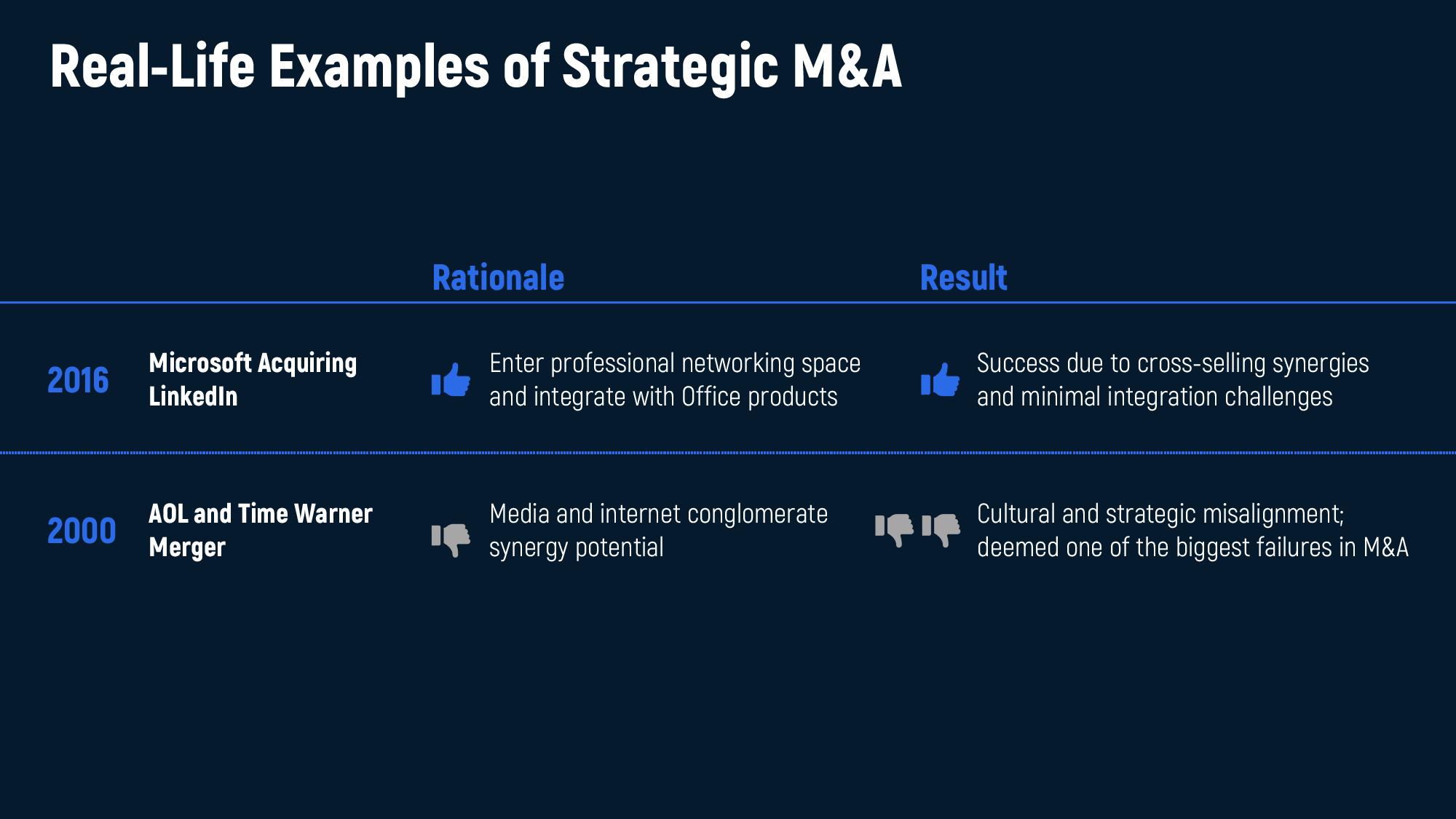

Microsoft – LinkedIn (2016, $26B)

- Rationale: Expand Microsoft’s ecosystem with a professional social network, strengthening its Office and cloud products.

- Outcome: Smooth integration, limited cultural clashes, and strong revenue synergies. LinkedIn has grown rapidly under Microsoft, becoming one of its most successful acquisitions.

Disney – Pixar (2006, $7.4B)

- Rationale: Revitalize Disney’s animation business and secure access to Pixar’s creative pipeline.

- Outcome: Massive success, generating billions in box office revenue and enabling cross-franchise expansion.

Interview angle: These examples highlight strategic fit and cultural alignment as drivers of success.

Failure stories

AOL – Time Warner (2000, $165B)

- Rationale: Combine internet distribution (AOL) with content (Time Warner).

- Outcome: One of the biggest failures in M&A history. Synergies never materialized, cultural clashes were severe, and the combined company lost massive value.

Daimler – Chrysler (1998, $36B)

- Rationale: Create a global auto giant with German engineering and U.S. scale.

- Outcome: Deep cultural misalignment, strategic conflicts, and eventual divestiture. The merger destroyed shareholder value.

Interview angle: Be ready to explain why these deals failed — usually overestimated synergies, culture clashes, or poor integration.

Conclusion: preparing for M&A interviews

M&A sits at the heart of investment banking — it combines strategy, finance, and execution in some of the most high-profile corporate decisions. For candidates, mastering the fundamentals is essential: you’ll be tested not only on definitions, but also on your ability to think like an advisor.

What interviewers look for

- Clear understanding of motivations – why buyers and sellers pursue deals.

- Knowledge of deal types – mergers, acquisitions, LBOs, tender offers.

- Familiarity with the M&A process – from sourcing to integration.

- Awareness of drivers and risks – synergies, overpayment, regulation, cultural fit.

- Commercial awareness – ability to cite real-world deals and explain their outcomes.

How to prepare effectively

- Learn the frameworks: Be able to walk through the M&A lifecycle step by step.

- Practice concise answers: Focus on 2–3 points per question, illustrated with examples.

- Stay updated on recent deals: Pick 2–3 current transactions and be ready to discuss rationale, valuation, and risks.

- Think like a banker: Always connect back to value creation for the client.

Final tip: Interviewers don’t expect you to be an M&A expert. They want to see structured thinking, commercial intuition, and confidence under pressure. If you can explain why deals happen, how they’re structured, and what can go right or wrong — you’ll stand out.