Introduction

If you’re preparing for a finance interview in 2025, whether it’s for investment banking, private equity, venture capital, or corporate finance—you will almost certainly face questions on Discounted Cash Flow (DCF) valuation. Recruiters love this topic because it tests not only your technical knowledge but also your ability to think like an investor.

A DCF model might sound intimidating at first. But once you break it down into clear steps, it becomes one of the most logical and structured ways to value a business. Unlike valuation methods based on multiples (such as P/E or EV/EBITDA), DCF is an intrinsic valuation approach—it looks at the company’s ability to generate future cash flows, rather than just comparing it to peers.

In this complete guide, you’ll learn:

- What a DCF model is and why it matters in interviews.

- The 6 simple steps to building a DCF from scratch.

- How to calculate Unlevered Free Cash Flows (UFCFs), Terminal Value, and WACC.

- The most common pitfalls and interview tips.

By the end of this article, you’ll not only know how to build a DCF model but also how to explain it confidently in an interview setting—a skill that can set you apart from other candidates.

What is a Discounted Cash Flow (DCF) model?

A Discounted Cash Flow (DCF) model is one of the most fundamental and widely used valuation methods in finance. It helps analysts and investors estimate the intrinsic value of a business or asset based on its future expected cash flows.

The logic is simple:

A company is worth the money it will generate in the future, adjusted to today’s value using a discount rate.

Why is it so important?

- It forces you to understand the business: revenues, costs, investments.

- It’s a standard tool in investment banking, private equity, venture capital, and corporate finance interviews.

- Unlike relative valuation (multiples), DCF is intrinsic – it values the company based on fundamentals, not market mood.

Key takeaway: DCF = Value of Future Free Cash Flows + Terminal Value, discounted back using WACC.

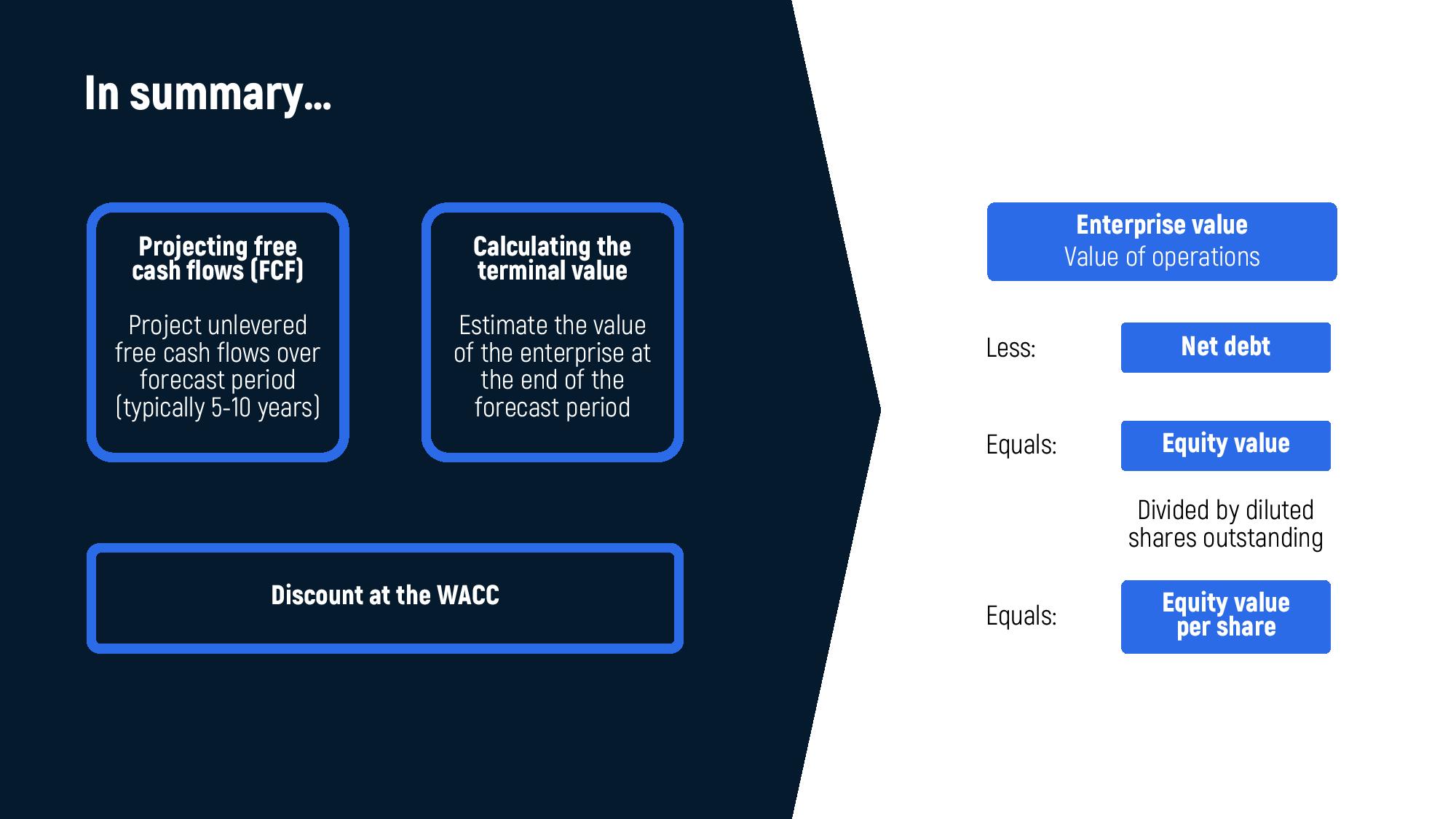

The 6 simple steps to build a DCF model

Building a DCF may sound intimidating, but it actually follows a clear, logical process. Here are the six steps you should always remember (and be ready to explain in an interview):

- Forecast Unlevered Free Cash Flows (UFCFs) – Estimate the company’s free cash flows for the next 5–10 years.

- Calculate terminal value – Estimate the value of the company beyond the forecast period.

- Discount UFCFs and Terminal Value to Present Value – Use WACC as the discount rate.

- Add non-operating assets – Cash or investments not related to core operations.

- Subtract net debt – Adjust for debt and liabilities.

- Divide by shares outstanding – Arrive at intrinsic value per share.

This structured approach ensures you don’t miss a step in valuation.

After providing this high-level overview, you should be ready to go deeper into each step if the interviewer asks. For example, they may follow up with questions about how to calculate terminal value, why WACC is used as the discount rate, or how to project free cash flows.

Later in this guide, we’ll explore the theory behind each step, and in a separate module, we will show you how to build a full DCF model in Excel.

Are You Ready for a Career a Top Company?

Answer three questions and get a personalized breakdown.

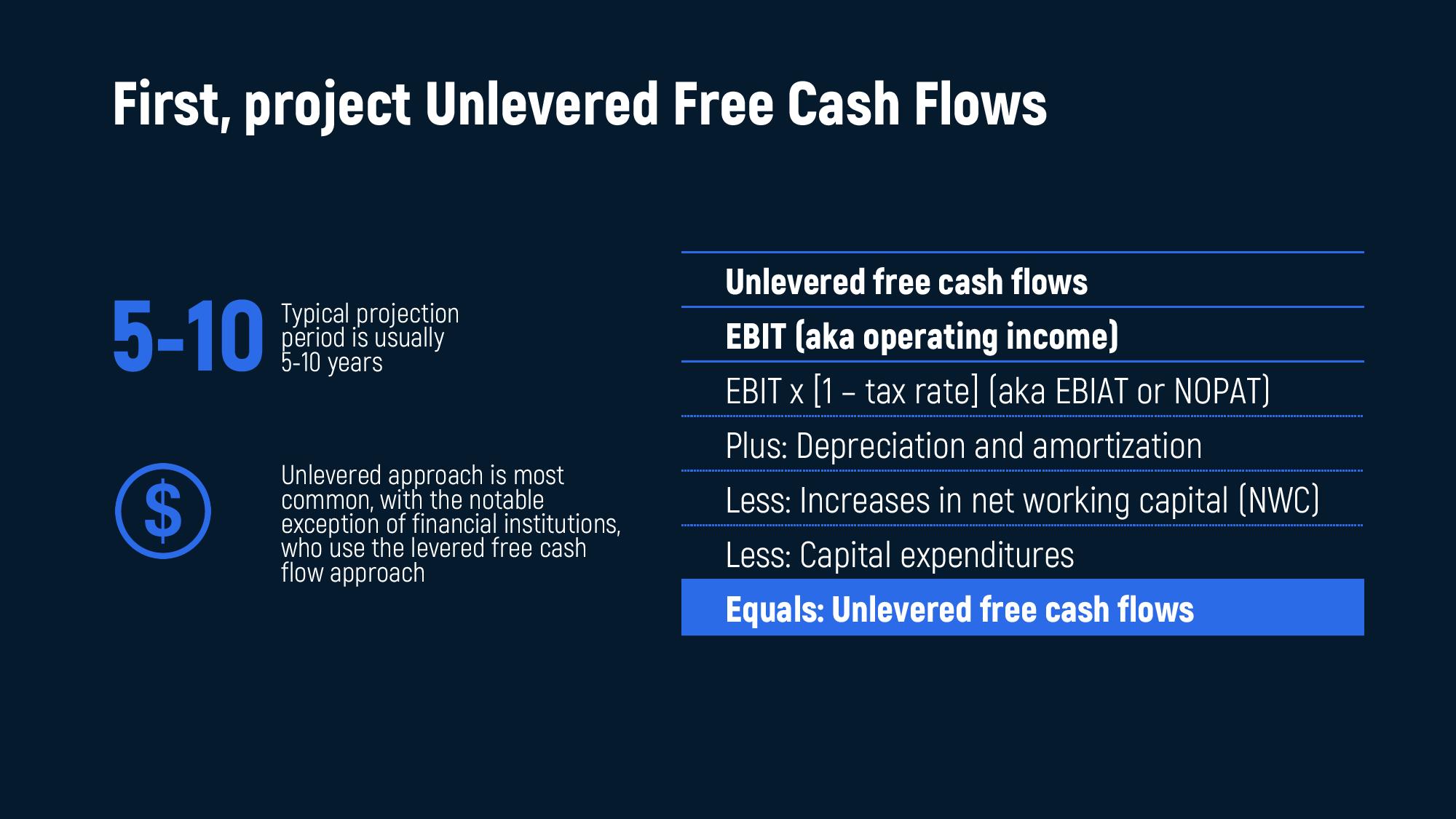

Step 1 – Forecasting free cash flows

The very first step of a DCF is projecting Unlevered Free Cash Flows (UFCFs), which represent the cash a company generates from its core operations before debt payments but after all reinvestments (CapEx and working capital).

The standard formula is:

UFCF = EBIT × (1 – Tax Rate) + D&A – Change in NWC – CapEx

Breaking this down:

- EBIT (Operating Income): Earnings before interest and taxes – the base for cash generation.

- (1 – Tax Rate): Adjusts EBIT to after-tax operating income (aka NOPAT).

- Depreciation & Amortization (D&A): Non-cash expenses added back.

- Change in Net Working Capital (ΔNWC): Increases = cash outflows; decreases = cash inflows.

- Capital Expenditures (CapEx): Investments needed to sustain growth.

Typical projection period: 5–10 years (longer projections become unreliable).

Why it matters:

- UFCFs show how much cash is available to both debt and equity investors.

- If UFCFs are wrong, your entire DCF falls apart.

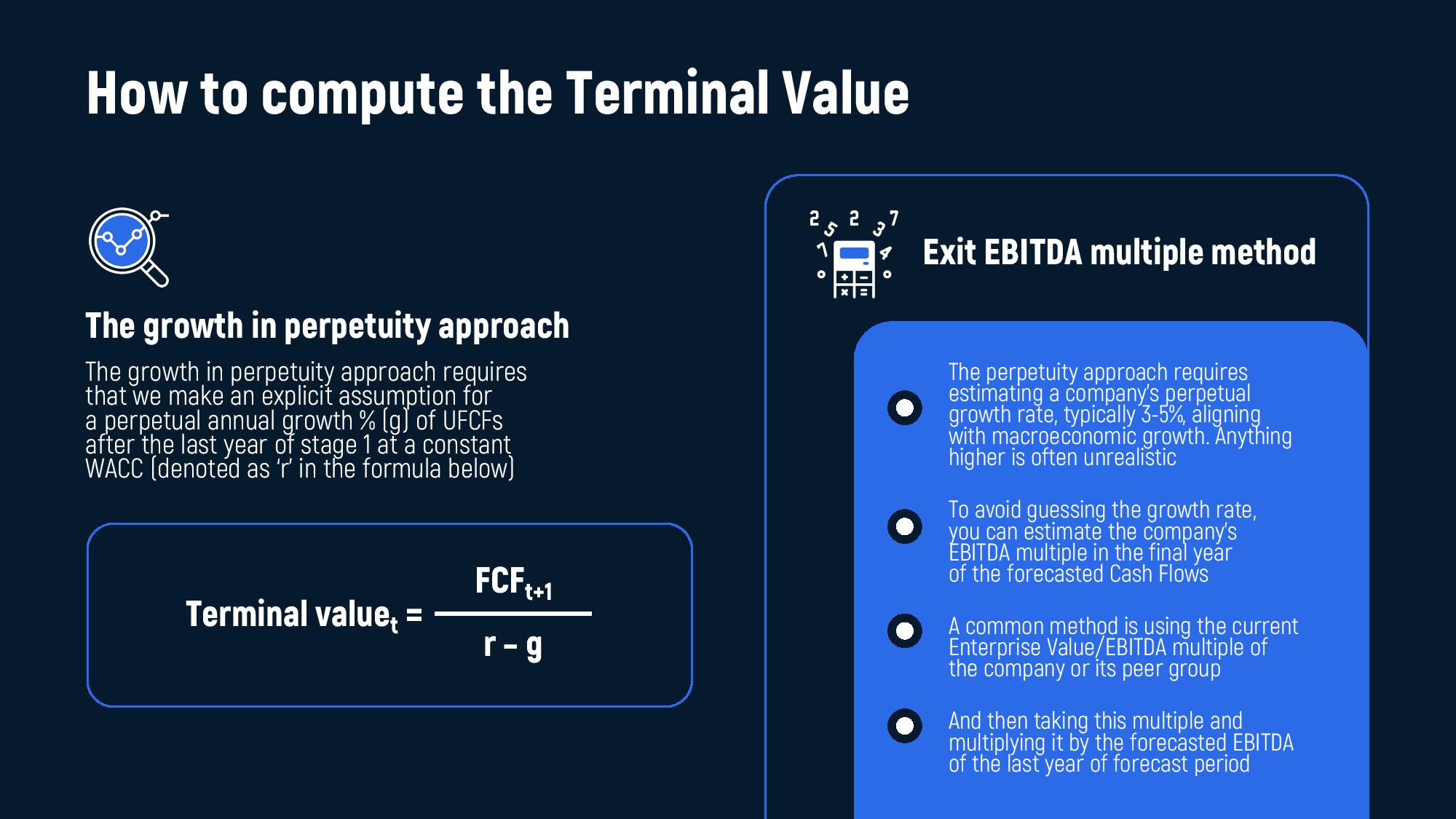

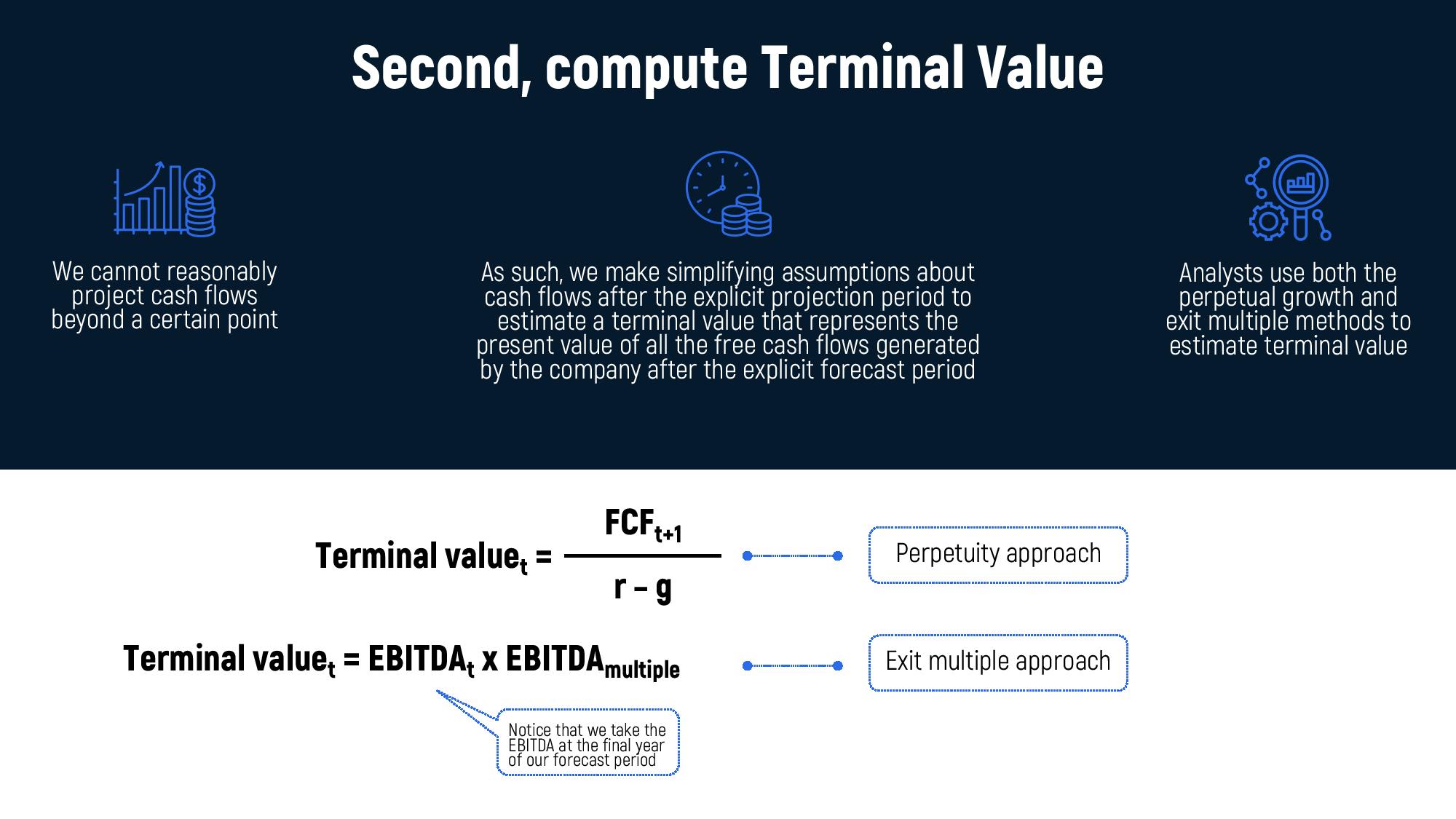

Step 2 – Computing the Terminal Value

When building a DCF, you usually forecast free cash flows for only 5–10 years. But businesses don’t just stop generating cash after that. To capture the value beyond the explicit forecast, we calculate a Terminal Value (TV).

Terminal Value represents the present value of all future cash flows beyond the forecast horizon. It often makes up over 50% of the total DCF value, which is why interviewers focus on whether you understand it.

There are two main approaches:

Perpetuity growth method (a.k.a. Gordon Growth Model)

TV =

FCFt+1r – g

- Assumes cash flows grow at a constant rate ggg forever.

- rrr = discount rate (WACC).

- ggg typically ranges from 2–3% in developed markets, aligned with long-term GDP growth.

Exit multiple method

TV = EBITDAt × Exit Multiple

- Uses an industry multiple (e.g., EV/EBITDA) applied to the company’s EBITDA in the final forecast year.

- Often based on current peer multiples or precedent transactions.

Key difference: The perpetuity method is more theoretical; the multiple method is more market-driven. In interviews, always mention both methods and their pros/cons.

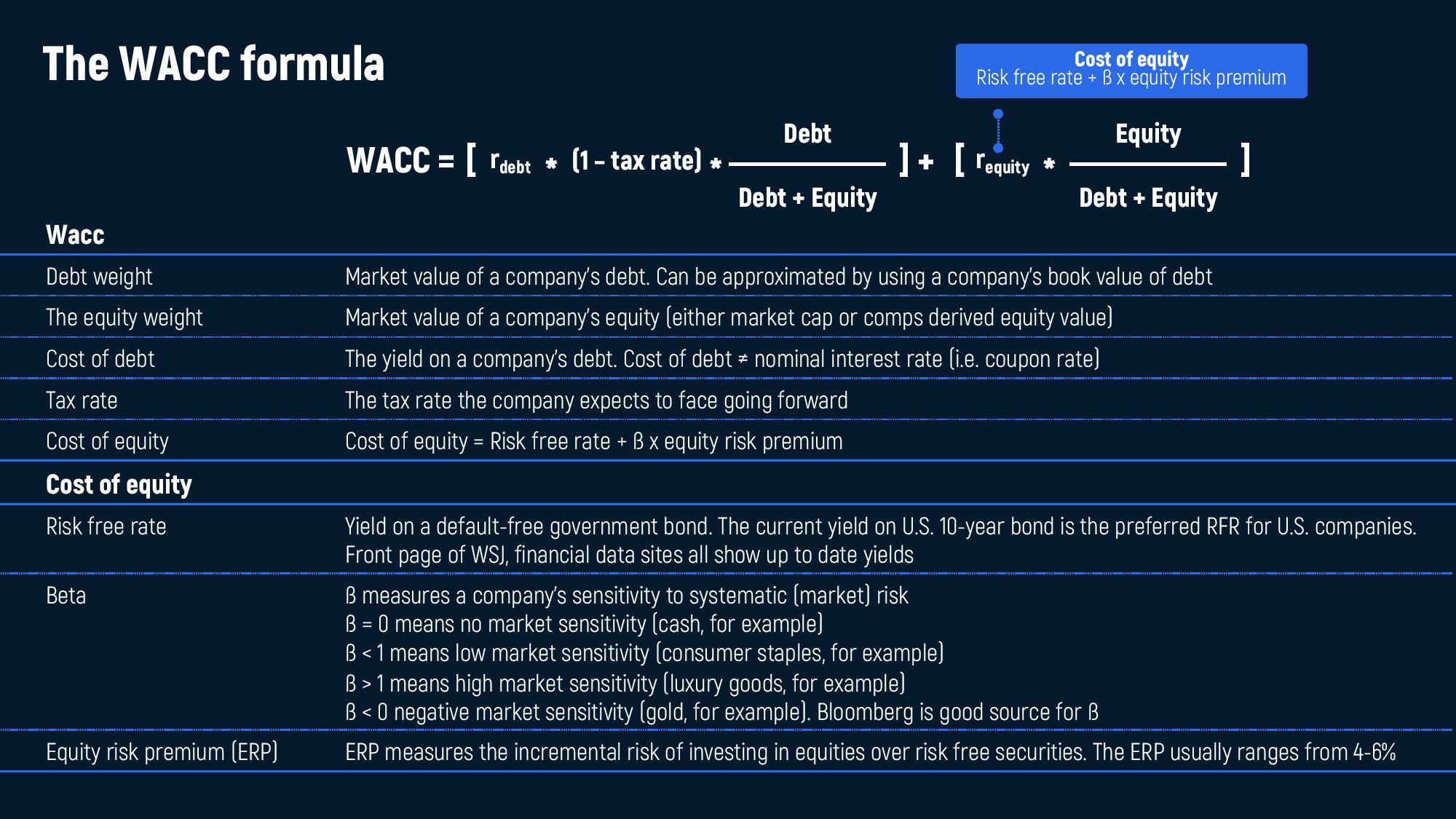

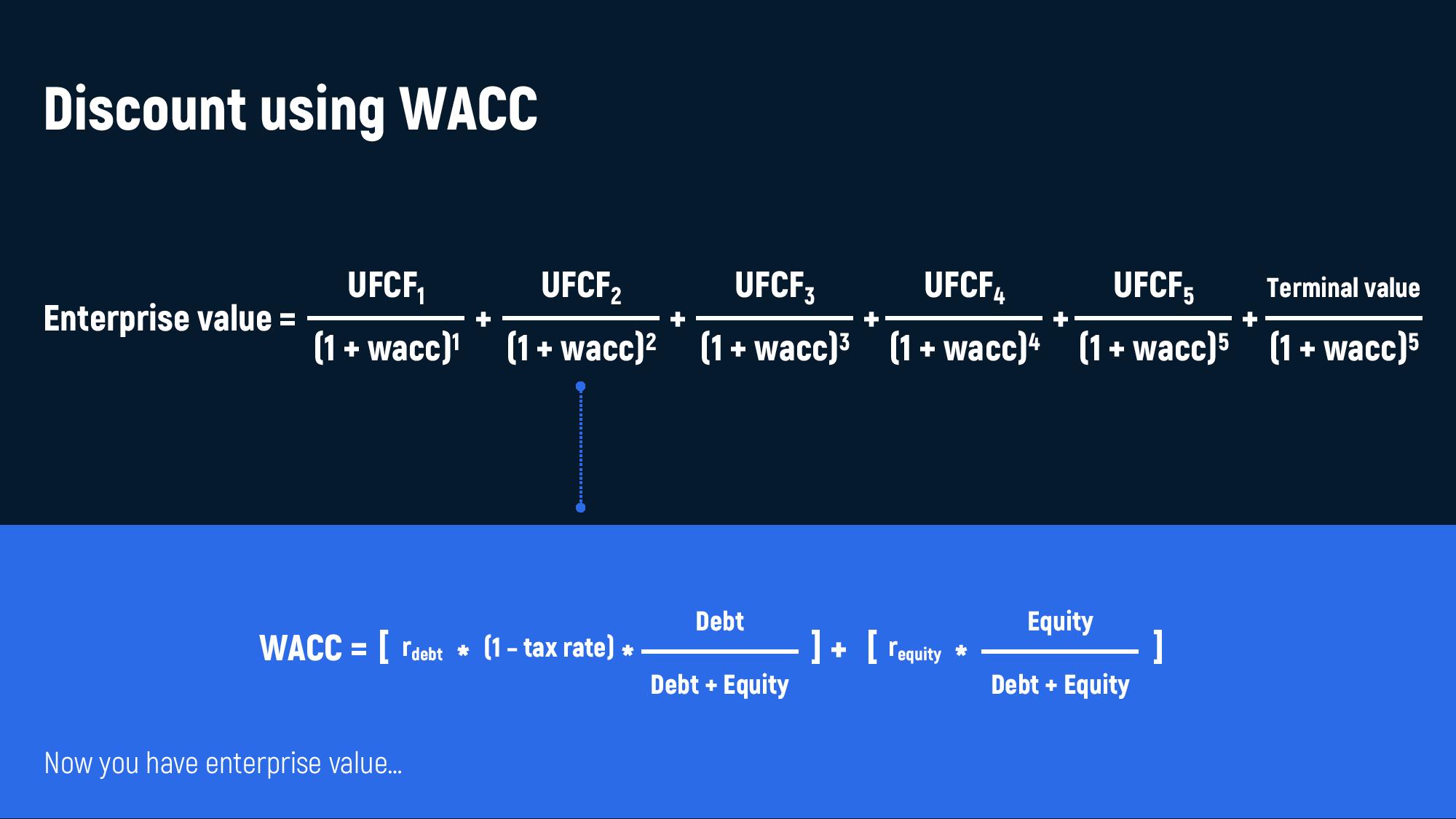

Step 3 – Discounting Cash Flows with WACC

Now that you have forecasted UFCFs and the Terminal Value, the next step is to bring them back to today’s value. This is done using the Weighted Average Cost of Capital (WACC).

Why WACC?

- WACC represents the average return required by both debt and equity investors.

- It reflects the risk profile of the business.

- Using WACC instead of an arbitrary discount rate ensures valuation is grounded in real financing costs.

The WACC formula

WACC = [rdebt × (1 – TaxRate) ×

DebtDebt + Equity

] + [ requity ×

EquityDebt + Equity

]

Where:

- Cost of debt (r debt): Interest rate a company pays on its borrowings. Adjusted for tax shield.

- Cost of equity (r equity): Calculated using the Capital Asset Pricing Model (CAPM):

requity = Risk Free Rate + β × Equity Risk Premium

Discounting the cash flows

The Enterprise Value is the sum of all discounted UFCFs plus the discounted Terminal Value:

EV =

UFCF1(1 + WACC)1

+

UFCF2(1 + WACC)2

+ … +

UFCFT(1 + WACC)T

+

TV(1 + WACC)T

The further into the future a cash flow is, the less it’s worth today.

Step 4 – Adding non-operating assets

Not all of a company’s value comes from its core operations. Some businesses hold significant non-operating assets such as:

- Cash & cash equivalents

- Short-term investments

- Equity stakes in other companies

These assets don’t directly generate operating cash flows but still add to shareholder value.

Example: If Apple has an enterprise value of $700B but holds $200B in cash, this cash must be added to the valuation.

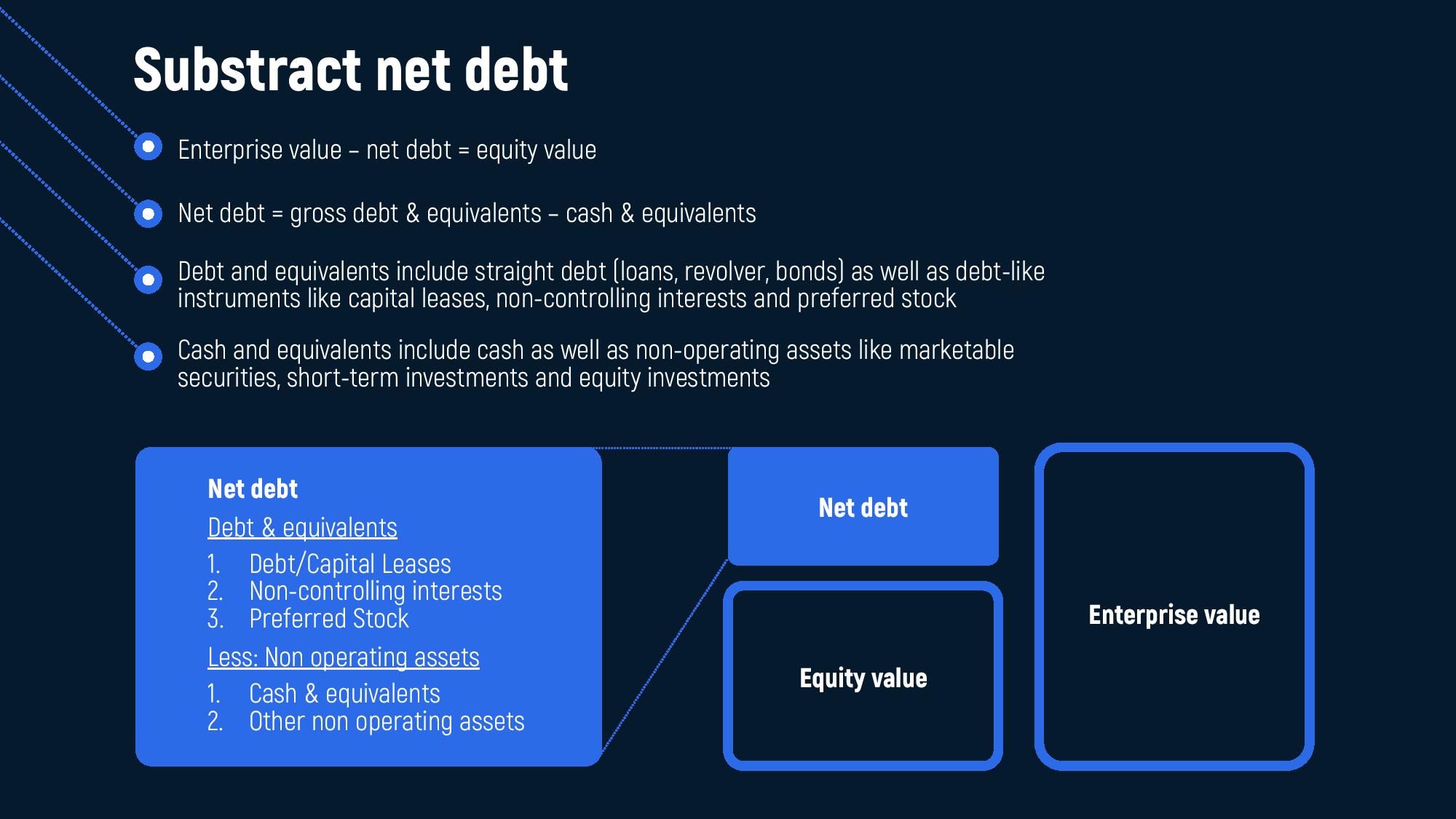

Step 5 – Subtracting net debt

After calculating the Enterprise Value (EV), the next step is to adjust for the company’s financing structure. Enterprise Value represents the value of the entire business (both debt and equity holders), but as equity investors, we are only interested in the portion left for shareholders.

That’s why we subtract Net Debt to arrive at Equity Value.

Equity Value = Enterprise Value + Cash & Non-Operating Assets – Debt

Where:

- Debt includes bonds, bank loans, leases, and sometimes preferred stock.

- Cash & equivalents reduce debt because they can be used to pay it down.

- Net Debt = Total Debt – Cash & Equivalents.

Example:

- Enterprise Value = $500M

- Cash = $50M

- Debt = $200M

- Equity Value = $500M + $50M – $200M = $350M

This ensures the DCF result reflects what actually belongs to shareholders after covering financial obligations.

Step 6 – Divide by shares outstanding

The last step in the DCF is moving from Equity Value to the Intrinsic Value per Share.

Intrinsic Value per Share =

Equity ValueDiluted Shares Outstanding

Key points for interviews:

- Always use diluted shares outstanding (which includes stock options, RSUs, convertible debt).

- The final number is the DCF-derived price per share.

- Compare it with the current market price to judge whether the stock is undervalued or overvalued.

Example:

- Equity Value = $350M

- Shares Outstanding = 50M

- Intrinsic Value per Share = $7.00

If the stock is currently trading at $5.00, the company appears undervalued.

Example: putting it all together

Now that we’ve gone through each step, let’s walk through a simple DCF example to see how everything connects. This is especially useful for interviews, where you may be asked to explain the DCF flow out loud.

Imagine we are valuing a company with the following inputs:

- Forecast horizon: 5 years

- UFCFs (in $m): 50, 60, 70, 80, 90

- WACC: 10%

- Terminal growth rate (g): 3%

- Net Debt: $200m

- Cash: $50m

- Shares Outstanding: 50m

Step 1 – Forecast UFCFs

We project free cash flows for the next 5 years.

👉 UFCFs = $50m, $60m, $70m, $80m, $90m

Step 2 – Compute Terminal Value

Using the Perpetuity Growth Method:

TV =

FCF6WACC – g

=

90 × (1 + 0.03)0.10 – 0.03

= 92.7 / 0.07 ≈ 1324m

Step 3 – Discount Cash Flows with WACC

Discount UFCFs and the Terminal Value back to present:

- PV of UFCFs = ~ $50 / 1.1 + 60 / 1.1^2 + … + 90 / 1.1^5 ≈ $260m

- PV of Terminal Value = $1324 / 1.1^5 ≈ $823m

- Enterprise Value (EV) = $260m + $823m = $1083m

Step 4 – Add non-operatinga assets

Cash balance = $50m

Adjusted EV = 1083 + 50 = 1133m

Step 5 – Subtract net debt

Debt = $200m

Equity Value = 1133 – 200 = 933m

Step 6 – Divide by shares outstanding

Intrinsic Value per Share =

93350

≈ $18.7

If the stock trades at $15 today, the DCF suggests it is undervalued.

Conclusion

The Discounted Cash Flow (DCF) model remains one of the most important tools in finance—both for real-world valuation and for interviews. While it can seem complex at first, breaking it down into six clear steps makes it far more approachable:

- Forecast UFCFs

- Compute Terminal Value

- Discount with WACC

- Add non-operating assets

- Subtract net debt

- Divide by shares outstanding

Mastering these steps will not only help you calculate the intrinsic value of a company, but also allow you to explain the logic clearly and confidently in interviews. Remember: the real challenge is not just plugging numbers into formulas—it’s defending your assumptions and showing that you understand the drivers of value.