Introduction

A Leveraged Buyout (LBO) is one of the most widely used strategies in private equity. In an LBO, a financial sponsor acquires a company primarily using borrowed funds, with the expectation that the company’s future cash flows will be sufficient to service the debt and ultimately generate attractive returns upon exit. Because leverage magnifies both gains and losses, not every business is a suitable buyout target.

Private equity firms spend significant effort identifying companies that can withstand the heavy debt burden typical of LBOs. They search for businesses with stable free cash flows, operational improvement potential, undervalued assets, and strong market positions. Without these traits, the risks of default or underperformance increase sharply.

Understanding what makes a company an ideal LBO candidate is crucial for several reasons:

- For private equity professionals, it guides deal sourcing and due diligence.

- For corporate managers, it highlights the qualities that increase attractiveness to financial sponsors.

- For students and candidates preparing for investment banking or PE interviews, it helps answer common technical and strategic questions.

In this article, we will:

- Explain the mechanics of an LBO and why candidate selection is critical.

- Outline the core characteristics of strong LBO targets.

- Provide examples of good vs bad candidates from real-world transactions.

- Discuss how these traits affect valuation, deal structuring, and returns.

By the end, you will have a clear framework for evaluating what makes a company a strong buyout candidate — whether in theory for interviews or in practice for private equity investing.

What is an LBO and why it matters

A Leveraged Buyout (LBO) is an acquisition strategy in which a private equity (PE) firm purchases a company using a combination of equity (their own capital) and a significant amount of debt financing. The acquired company’s future cash flows are then used to pay down the debt over time.

How it works

- Acquisition: A PE firm identifies a target company and finances the purchase largely with borrowed money.

- Ownership: After the deal, the company is privately owned and responsible for repaying the debt.

- Value Creation: The PE firm improves the company through operational efficiencies, strategic initiatives, or restructuring.

- Exit: After several years, the PE firm sells the company (via IPO, secondary buyout, or strategic sale) at a higher valuation, generating returns.

Why it matters

- Leverage amplifies returns: Using debt reduces the equity investment required, so if the company grows or stabilizes, returns on equity can be very high.

- But leverage also amplifies risk: If cash flows are unstable, the company may default, making candidate selection critical.

- PE firms’ goal: Acquire, improve, and exit — not just through financial engineering, but by driving operational value creation.

Core characteristics of an ideal LBO candidate

Not every company can handle the debt load of an LBO. Private equity firms look for specific qualities that reduce risk and maximize potential upside. These characteristics define what makes a business an attractive buyout target.

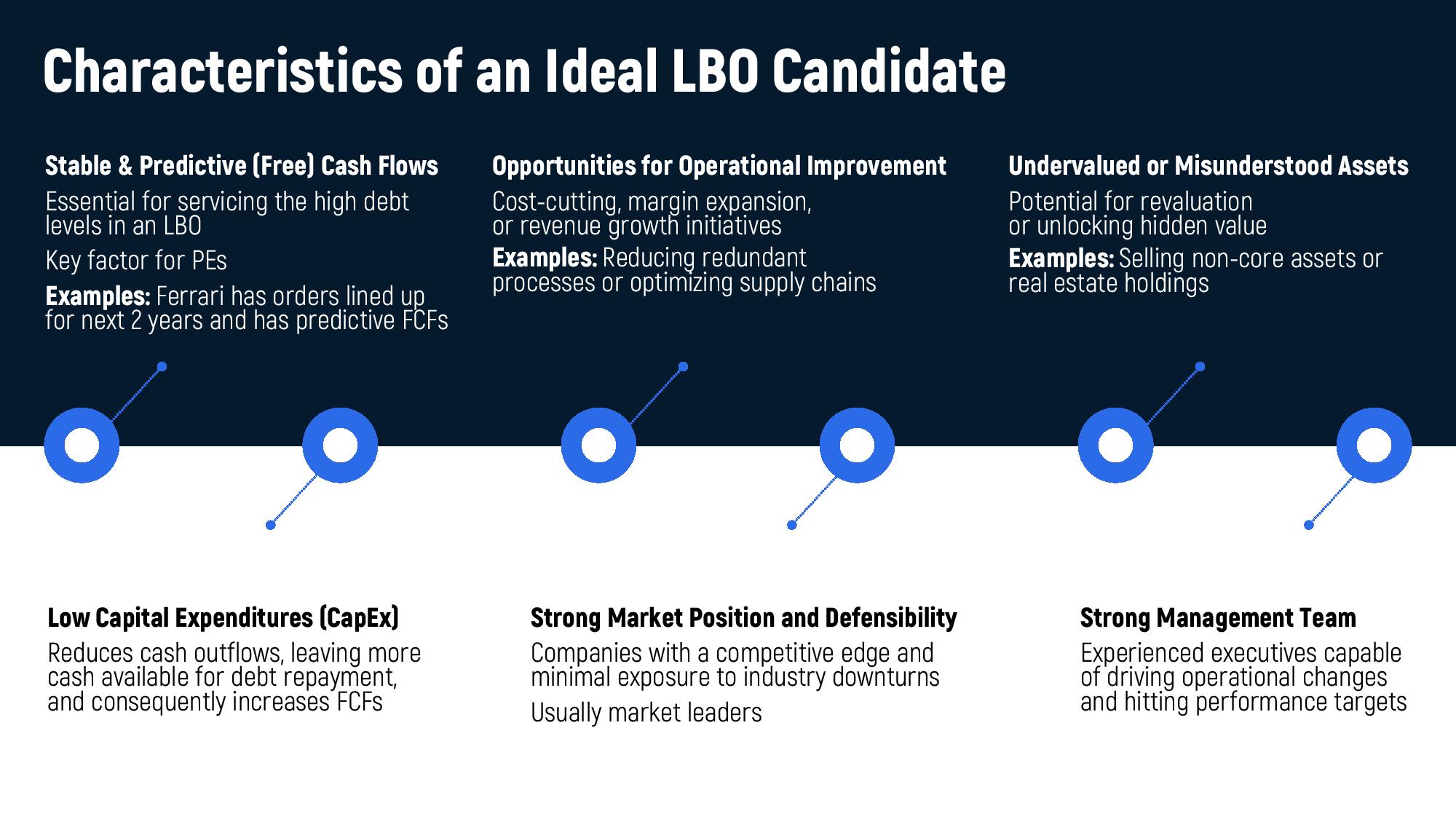

1. Stable & Predictive free cash flows

- Why it matters: Debt in an LBO is repaid through cash flows, so stability and predictability are essential.

- Example: A company with recurring revenues from long-term contracts (e.g., Ferrari with orders secured for years ahead).

2. Opportunities for operational improvement

- Why it matters: PE firms create value by improving efficiency, cutting costs, or growing revenues.

- Example: Streamlining supply chains, reducing redundant processes, or launching pricing initiatives.

3. Undervalued or misunderstood assets

- Why it matters: Assets that are overlooked by the market can be sold or restructured to unlock value.

- Example: Divesting non-core divisions or monetizing real estate holdings.

4. Low Capital Expenditures (CapEx)

- Why it matters: Lower ongoing CapEx means more cash is available for debt repayment.

- Example: Asset-light service businesses often have stronger LBO profiles than heavy industrials.

5. Strong market position & defensibility

- Why it matters: Companies with leading market positions, competitive advantages, and resistance to downturns provide downside protection.

- Example: Market leaders with high switching costs or strong brand loyalty.

6. Strong management team

- Why it matters: Operational improvements and performance targets depend on execution. Experienced management teams increase the likelihood of success.

Examples of good vs bad LBO candidates

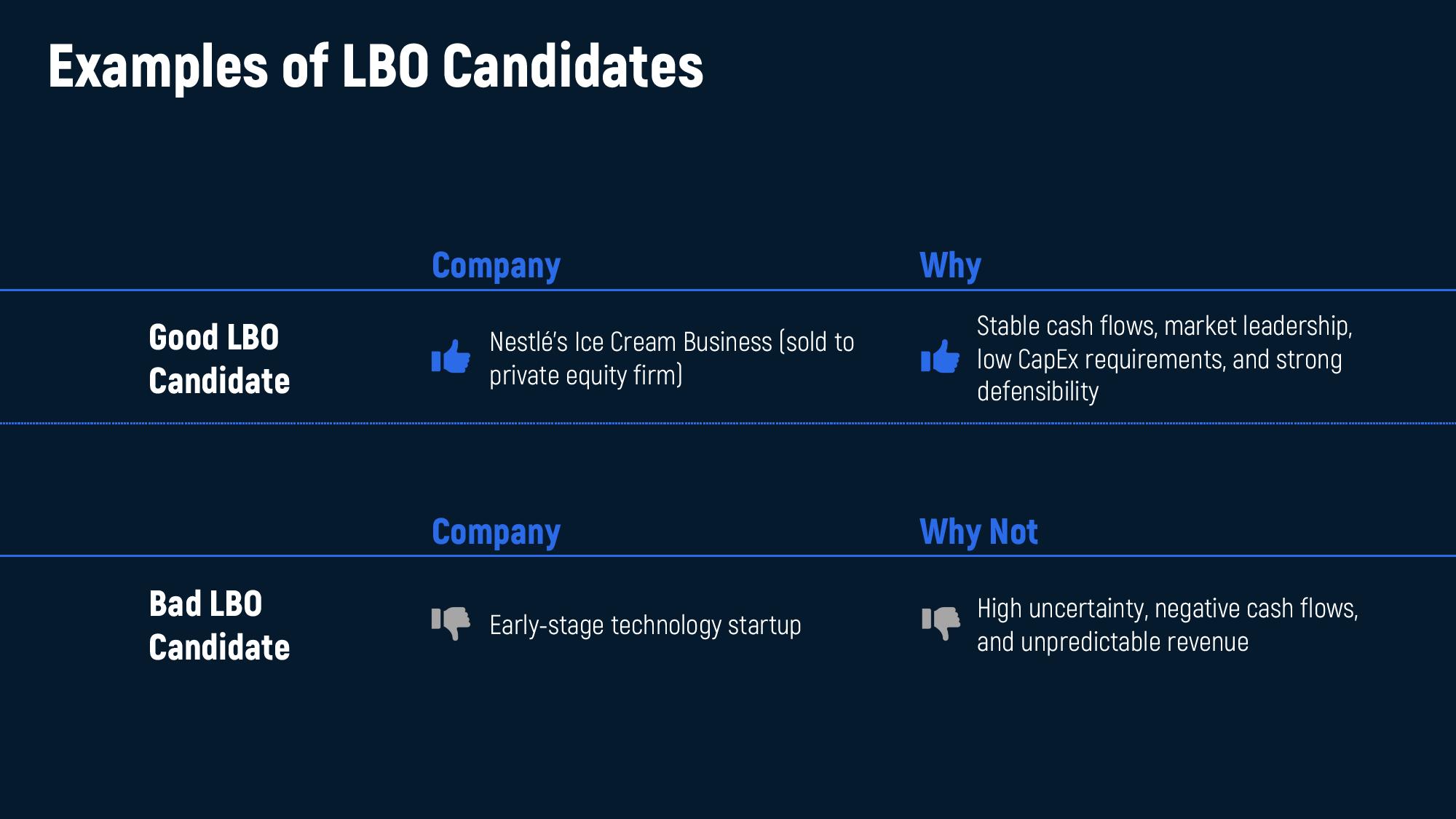

The best way to understand what makes a company a strong LBO target is to compare examples.

Take Nestlé’s Ice Cream Business. It generates steady and predictable cash flows, has a strong market position, and requires relatively low capital expenditures to operate. These qualities make it an attractive candidate for a leveraged buyout because private equity investors can rely on consistent earnings to service debt while also finding opportunities to optimize costs and operations.

Now contrast this with an early-stage technology startup. Despite rapid growth potential, the company has negative or highly volatile cash flows, uncertain profitability, and significant reinvestment needs. Such a business would struggle under the weight of heavy debt financing. For private equity firms, the risk of default is far greater than the potential reward, making it a poor LBO candidate.

These examples highlight a key principle: predictability and stability outweigh hype and high growth potential. Private equity firms are not simply chasing fast-growing companies; they are looking for businesses that can generate reliable free cash flow and sustain leverage over time.

Implications for valuation and deal structuring

The traits that define a strong LBO candidate not only make a company attractive but also shape how much debt it can take on, what valuation it commands, and how investors plan their exit.

- Leverage capacity:

Companies with stable cash flows and defensible market positions can safely carry higher levels of debt. Lenders are more willing to provide financing when repayment is predictable. Volatile businesses, on the other hand, are restricted to lower leverage, limiting the returns private equity firms can achieve. - Valuation multiples:

Strong LBO candidates often trade at higher multiples because of their reliability and free cash flow generation. For PE firms, paying a premium is acceptable if it reduces risk and supports stable debt repayment. In contrast, businesses with weak or uncertain earnings may appear “cheap,” but they rarely work as LBOs since their cash cannot support the structure. - Exit options:

Candidate quality also influences the exit strategy. Companies with stable earnings and improved operations under PE ownership are more attractive to strategic buyers, secondary buyout funds, or public investors via IPO. Weak candidates may struggle to find interested buyers, even if acquired at a discount.

In short, the strength of the target company determines how the deal is financed, how much can be paid upfront, and what exit opportunities exist.

Are You Ready for a Career a Top Company?

Answer three questions and get a personalized breakdown.

Common misconceptions about LBO candidates

When people first learn about leveraged buyouts, they often make assumptions about what kinds of companies are attractive targets. Many of these assumptions are misleading. Let’s clear up the most common misconceptions.

- Myth: Only high-growth companies make good LBO candidates.

Reality: Growth is not required — in fact, it often adds risk. What matters most is predictable free cash flow that can cover debt obligations. - Myth: Any undervalued company is a strong LBO opportunity.

Reality: Cheap valuation alone isn’t enough. If a business doesn’t generate reliable cash flow, its low price won’t prevent default under heavy leverage. - Myth: LBOs are only about cost-cutting.

Reality: While operational efficiencies are important, private equity firms also create value through revenue growth, strategic repositioning, and better capital allocation. - Myth: Capital-intensive companies can be strong candidates if their markets are attractive.

Reality: Heavy CapEx requirements reduce available free cash flow, making it harder to service debt and less suitable for an LBO.

These misconceptions highlight the key lesson: LBOs are not about chasing growth or bargains — they are about finding stable, cash-generating businesses that can handle leverage.

Conclusion

A successful leveraged buyout depends less on financial engineering and more on the fundamentals of the target company. Private equity firms search for businesses that can sustain debt and still deliver attractive returns — and that requires a very specific profile.

The strongest LBO candidates are those with stable and predictable free cash flows, low capital expenditure needs, and defensible market positions. Additional value comes from opportunities for operational improvement, hidden or undervalued assets, and the presence of an experienced management team capable of executing change.

Case comparisons, such as Nestlé’s Ice Cream Business versus an early-stage technology startup, underline the key lesson: predictability and stability matter more than rapid growth or hype. Without reliable cash generation, leverage becomes a liability rather than a tool.

These qualities influence not just target selection but also how deals are structured and valued. Strong candidates support higher leverage, command investor confidence, and offer multiple exit routes — from strategic sales to IPOs. Weak candidates, even if cheap, often fail under the weight of debt.

For professionals in private equity, corporate finance, and investment banking, understanding what makes a company buyout-ready is essential. For students and interview candidates, it’s a fundamental framework that shows you can think like an investor.