Introduction

In the world of mergers and acquisitions (M&A), synergies are the magic word everyone talks about — the idea that two companies together are worth more than the sum of their parts. They are the foundation of almost every deal pitch, investment case, and M&A interview question.

If you’re just starting to explore how M&A deals work from start to finish, check out The Ultimate M&A Guide for Aspiring Investment Bankers 2025 — it’s a great companion resource that covers the entire process, from deal sourcing to post-merger integration.

In simple terms, synergies represent the additional value created when two companies combine. This value can come from increased revenue opportunities, lower costs, or operational efficiencies that wouldn’t exist if the firms remained separate. When modeled correctly, synergies can transform a borderline acquisition into a value-creating transaction — but when overestimated, they can destroy shareholder value and deal credibility.

That’s why understanding synergies is crucial for anyone preparing for investment banking, private equity, or corporate finance interviews. Interviewers use synergy questions to test your ability to:

- Break down complex concepts into clear categories (revenue vs cost synergies).

- Think critically about deal logic and integration challenges.

- Link strategic reasoning to financial impact in valuation and accretion/dilution models.

In this guide, we’ll cover everything you need to master the topic:

- What M&A synergies are and how they’re calculated.

- The difference between revenue and cost synergies — with real examples.

- Why synergies are often overestimated in practice.

- And how they affect deal valuation and EPS accretion/dilution in interview cases.

By the end, you’ll have a complete framework to confidently explain synergies in both qualitative discussions and technical modeling questions, just like a top-tier investment banking candidate.

If you’re new to investment banking and want to understand how the industry works before diving into deal mechanics, start with Investment Banking: What It Is, How It Works, and How to Start — it provides a clear overview of the role bankers play in M&A transactions.

What are synergies in M&A?

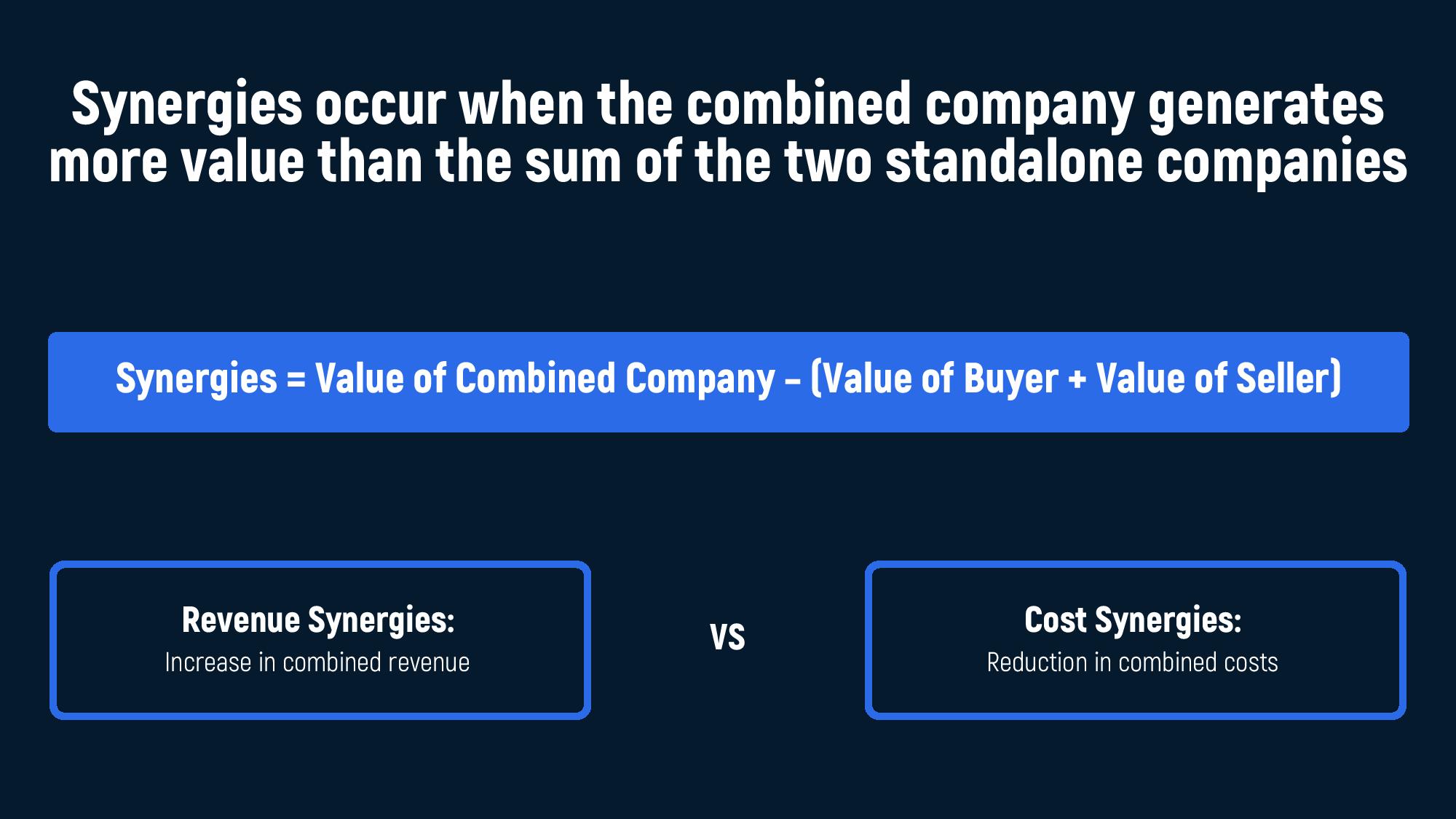

At the core of every merger or acquisition lies a simple goal: to create value greater than what the two companies could achieve individually. That additional value is known as a synergy.

In financial terms, synergies are expressed through the formula:

Synergies = Value of Combined Company − (Value of Buyer + Value of Seller)

If the combined company is worth more than the sum of its parts, the difference represents the synergistic value created through the deal. This is what justifies paying a premium to acquire another firm.

Why synergies matter

Synergies are the key justification behind M&A activity. They explain why a deal makes sense — not only from a strategic standpoint but also from a financial one. Analysts model synergies to see whether a deal creates shareholder value, increases earnings per share (EPS), or improves margins and returns.

However, not all synergies are created equal. In most cases, value creation comes from two primary sources:

1. Revenue synergies

Revenue synergies refer to new or increased revenue opportunities that result from the merger. They arise when the combined company can generate more sales than the two firms could independently.

Examples include:

- Cross-selling: selling one company’s products to the other’s customer base.

- Geographic expansion: using the partner’s distribution channels to enter new markets.

- Product bundling: combining complementary products into a single offering.

Revenue synergies are often highlighted in pitch books but are harder to quantify and slower to realize, as they depend on market response and successful integration.

2. Cost synergies

Cost synergies come from reducing expenses after the merger by eliminating duplication and improving efficiency. They tend to be easier to measure and faster to implement.

Examples include:

- Consolidating overlapping departments or production facilities.

- Reducing headcount in back-office operations.

- Negotiating better prices from suppliers due to increased scale.

Cost synergies are typically the main driver of short-term deal value, especially in large-scale mergers.

Together, revenue and cost synergies explain where the incremental value of an M&A deal comes from. The best analysts, and interview candidates, don’t just name them; they can link them to specific financial outcomes, such as higher EBITDA, improved margins, or enhanced EPS.

Revenue synergies explained

Revenue synergies are the most exciting — and often the most debated — part of any merger or acquisition. They represent the growth potential that emerges when two companies combine: the ability to sell more products, reach more customers, or enter new markets together.

In theory, revenue synergies sound simple. In practice, they’re hard to quantify and even harder to achieve — which is exactly why interviewers love to test your understanding of them.

What are revenue synergies?

Revenue synergies occur when the combined company generates higher revenue than the two firms could independently. The logic is that each company brings something valuable to the table: distribution networks, customer bases, brand strength, or complementary products. When merged, these assets reinforce one another and expand the revenue potential.

Formally, revenue synergies can be expressed as:

Revenue Synergies = Revenue of Combined Company − (Revenue of Buyer + Revenue of Seller)

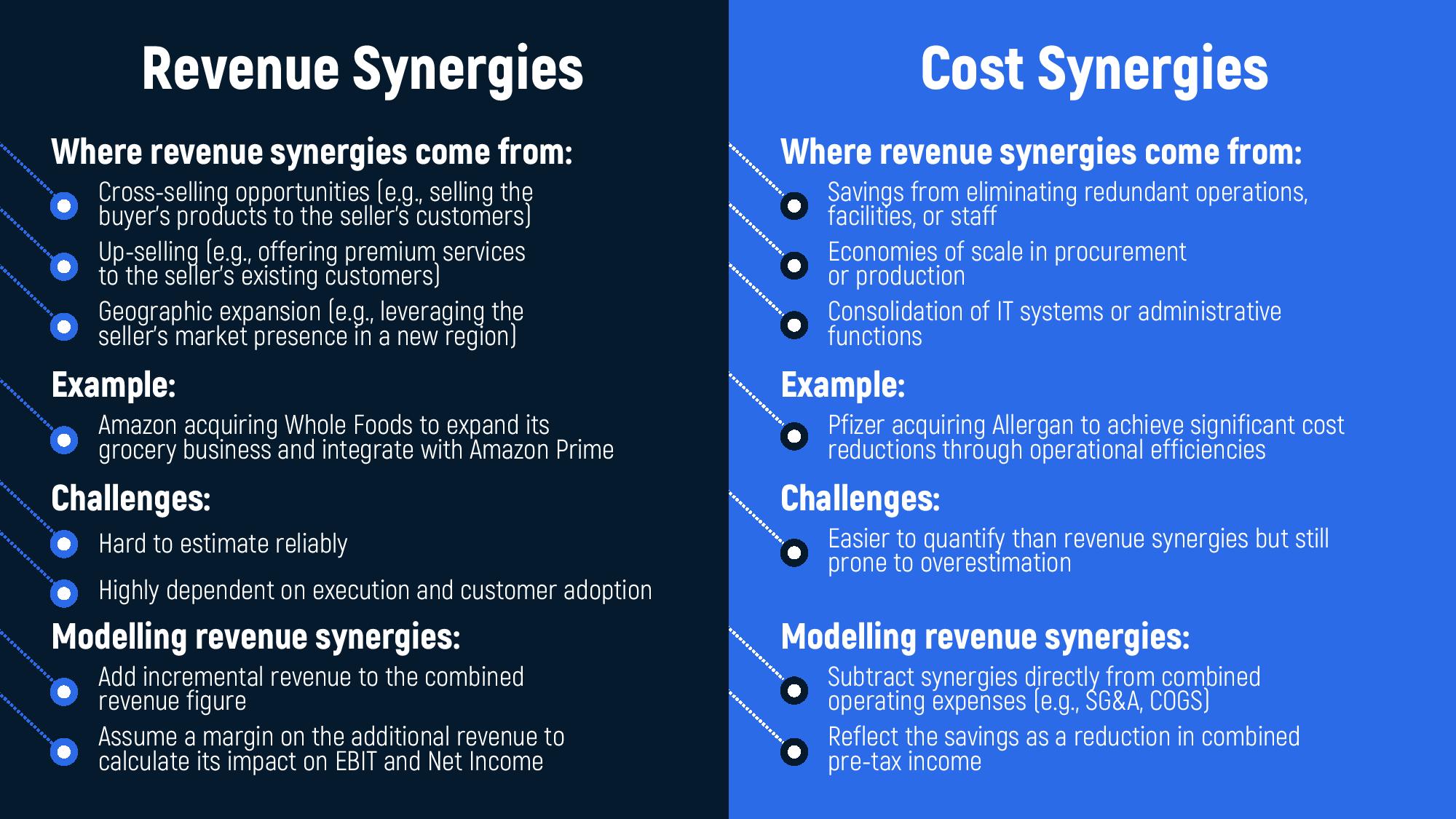

Common Sources of Revenue Synergies

The main sources you should know, and mention in interviews, include:

- Cross-Selling: Selling one company’s products to the other’s customer base.

Example: Microsoft acquiring LinkedIn — integrating LinkedIn data into Microsoft’s CRM products. - Up-Selling: Encouraging customers to purchase higher-value or premium versions of products.

Example: Disney acquiring 21st Century Fox — enabling Disney+ to offer a broader premium content library. - Geographic Expansion: Leveraging existing distribution networks to enter new regions.

Example: A European consumer brand acquiring an Asian competitor to access new markets faster. - Product Bundling: Combining complementary products into a single offering.

Example: A telecom company bundling mobile, internet, and streaming services after acquiring a content provider.

How to model revenue synergies

When discussing modeling in interviews, keep it simple and structured:

- Estimate incremental revenue (e.g., +5% sales growth from cross-selling).

- Apply an expected EBIT margin (since revenue synergies flow through the income statement).

- Calculate the impact on EBIT and Net Income to measure accretion/dilution.

This method shows that you understand both the strategic logic and financial translation of synergies — a key interview skill.

Challenges in realizing revenue synergies

While attractive on paper, revenue synergies are notoriously hard to achieve.

They depend on:

- Smooth integration of sales teams and systems.

- Customer acceptance of new or bundled products.

- Time — revenue growth often takes 2–3 years post-merger to materialize.

This is why many analysts discount revenue synergy projections in financial models by 25–50%, especially in early deal stages.

Real-world example

Consider Amazon’s acquisition of Whole Foods:Amazon leveraged its e-commerce platform and customer base to increase in-store traffic and online grocery sales. That’s a textbook example of revenue synergies through channel integration.

Are You Ready for a Career a Top Company?

Answer three questions and get a personalized breakdown.

Cost synergies explained

While revenue synergies often make headlines, it’s cost synergies that form the backbone of most M&A value creation. They are tangible, measurable, and typically realized faster after a deal closes.

In interviews, candidates who can clearly explain cost synergies, where they come from, how they’re modeled, and what risks they carry, demonstrate a strong grasp of M&A fundamentals.

What are cost synergies?

Cost synergies are the savings achieved when two companies combine and eliminate overlapping costs. These savings result from streamlining operations, consolidating teams, and leveraging economies of scale.

Formally:

Cost Synergies = Costs of Buyer + Costs of Seller − Costs of Combined Company

The goal is simple — to operate more efficiently together than apart.

Common sources of cost synergies

Here are the main drivers you should know and mention confidently in interviews:

- Headcount Reduction: Removing overlapping roles, especially in sales, marketing, or administration.

Example: After the merger of Exxon and Mobil, back-office and regional operations were consolidated to reduce overhead. - Procurement and Supplier Savings: Larger companies can negotiate better pricing with suppliers due to higher purchasing volumes.

Example: Kraft and Heinz achieved substantial procurement synergies post-merger by combining supply chains. - Facility Consolidation: Closing duplicate offices, factories, or distribution centers.

Example: Bank mergers often involve branch rationalization to cut fixed costs. - IT and Infrastructure Integration: Combining systems, platforms, and logistics networks to avoid redundancies.

- Shared Services Optimization: Streamlining HR, accounting, and legal teams across both entities.

How to Model Cost Synergies

Cost synergies are relatively straightforward to model:

- Identify expected annual cost savings (e.g., $50M per year).

- Apply them directly to the income statement under SG&A or COGS.

- Assume a realization timeline — typically 1–3 years post-closing.

- Subtract integration costs (one-time expenses to achieve the savings).

The net result is an increase in EBIT and pre-tax income, making the deal more accretive.

Real-world example

A clear example is Pfizer’s acquisition of Allergan, where the combined company expected billions in cost savings by consolidating R&D, manufacturing, and administrative operations. These efficiencies directly improved margins and cash flow projections, justifying the high acquisition premium.

Why cost synergies matter

- They’re more credible and quantifiable than revenue synergies.

- They deliver immediate EPS impact, improving accretion/dilution outcomes.

- They’re a key focus in due diligence and integration planning.

However, they can’t be taken for granted. Integration delays, employee turnover, or system incompatibility can reduce expected savings.

Why synergies are often overestimated

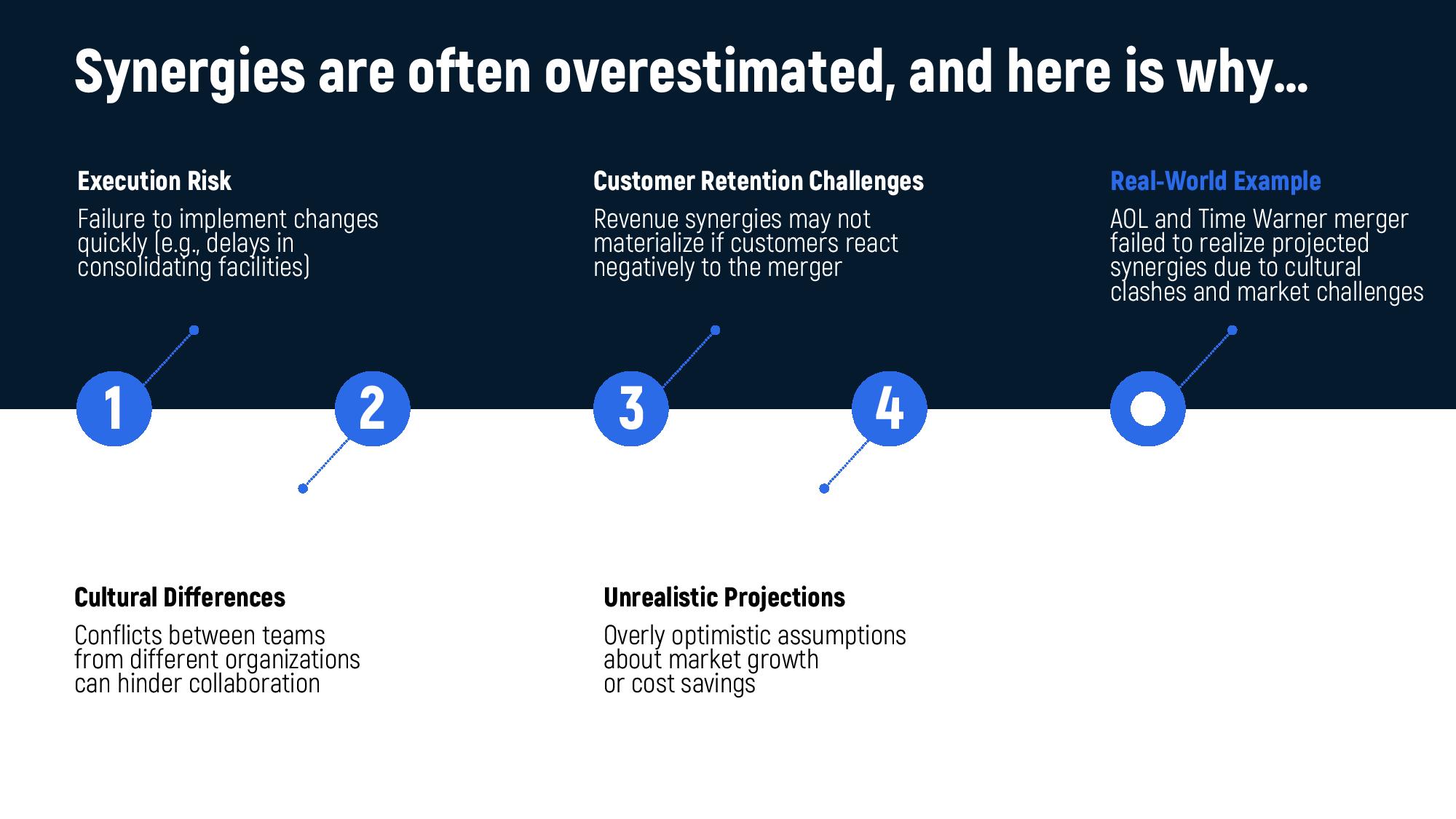

In M&A, it’s common for management teams and bankers to promise massive synergies to justify high deal premiums. But in reality, many of those projected synergies never materialize. Overestimating synergies is one of the most frequent, and most expensive, mistakes in corporate finance.

For interviewers, this topic tests whether you can think critically about deal assumptions and execution risks — not just recite definitions.

1. Execution risk

Even if the logic behind the synergy is sound, execution failures often derail it. Integrating two large organizations takes time, coordination, and resources. Delays in combining teams, systems, or operations can reduce or completely erase expected savings.

Example: If a merger aims to save $100M through staff reductions, but restructuring takes 2–3 years instead of one, those savings may arrive too late to justify the deal premium.

2. Cultural and organizational differences

Merging two corporate cultures can be harder than merging two balance sheets.

Different management styles, communication systems, and incentive structures can slow decision-making and reduce collaboration.

Example: The AOL–Time Warner merger (2000) failed largely due to cultural misalignment — media executives and tech entrepreneurs struggled to integrate, and synergy forecasts collapsed.

3. Customer and market reaction

Companies often underestimate the reaction of customers and competitors. Integration can disrupt service, alienate clients, or provoke aggressive responses from rivals. Revenue synergies, in particular, depend heavily on customer retention and adoption — both of which can decline post-merger.

4. Overly optimistic assumptions

Sometimes synergy forecasts are simply too optimistic. Analysts may assume unrealistic growth rates or cost reductions without accounting for friction, delays, or redundancy costs.

While synergy announcements excite investors initially, under-delivery later can erode market confidence.

Example: The HP–Compaq merger (2002) promised $2.5B in annual synergies but delivered only a fraction due to slower integration and revenue loss.

5. Integration costs often ignored

One-time expenses, severance packages, system upgrades, rebranding, and legal costs, are often overlooked. These costs can significantly offset expected synergy gains, especially in the first year after a merger.

The takeaway

Overestimating synergies doesn’t just hurt credibility — it can destroy shareholder value.

A realistic synergy model should always include:

- Conservative assumptions,

- Phased implementation, and

- A clear timeline for realization.

Synergies in accretion/dilution analysis

In M&A interviews, and in real transactions, you’ll often be asked how synergies affect accretion/dilution analysis. This question tests whether you can translate strategic reasoning into financial impact.

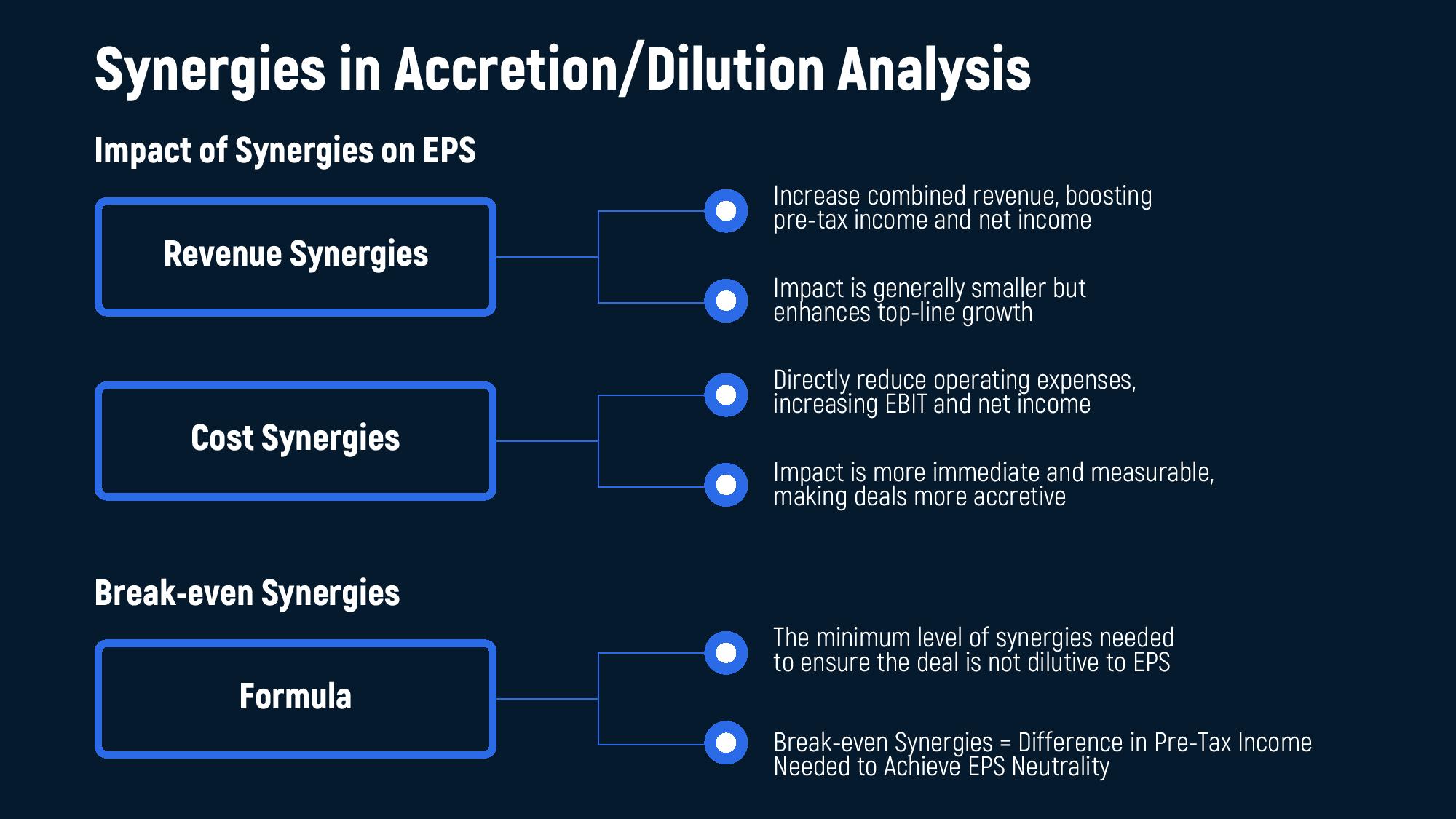

Accretion/dilution analysis measures how an acquisition affects the buyer’s earnings per share (EPS) after the deal closes. If EPS increases, the deal is accretive; if it decreases, it’s dilutive.

And synergies often make the difference between the two.

How synergies impact EPS

Synergies improve post-deal earnings by boosting revenue and/or reducing costs.

- Revenue synergies: Increase the combined company’s top line and profit margins. They improve EPS gradually, as the new revenue takes time to materialize.

- Cost synergies → Decrease SG&A or production costs. They have an immediate effect on profitability, making the deal more accretive in the short term.

In most M&A models, cost synergies drive early EPS accretion, while revenue synergies are treated as longer-term upside.

Example: modeling synergy impact

Let’s say Company A acquires Company B.

- Without synergies, the deal is slightly dilutive (EPS decreases by 2%).

- After modeling $50M in annual cost savings (cost synergies), net income rises enough to turn the deal EPS-neutral or even accretive.

This example shows how synergy assumptions can directly shift the outcome of accretion/dilution analysis — which is why they’re carefully scrutinized by both investors and deal teams.

Break-even synergies

Analysts often calculate the level of synergies needed to make a deal EPS-neutral. This is known as the break-even synergy level — the point at which additional earnings from synergies offset the dilution from financing costs or share issuance.

Break-even Synergies = Incremental Pre-Tax Income Needed to Achieve EPS Neutrality

This figure helps evaluate deal risk:

- If only modest synergies are required to break even, the deal is lower risk.

- If massive synergies are required, the deal’s success depends heavily on execution.

Why synergy assumptions matter

- Optimistic synergy forecasts can make an expensive deal look accretive — but reality might tell a different story post-closing.

- Conservative synergy modeling improves credibility, especially when presenting to investors or in interview answers.

- In both cases, the logic must connect — strategic synergies must translate to measurable financial outcomes.

If you’re exploring where mastering these concepts can take you, check out The Ultimate Guide to the Investment Banking Career Path: Roles, Salaries, and Growth 2025 — it breaks down what each role in investment banking actually does, how compensation grows, and how M&A skills fit into long-term career development.

Interview tip:If asked “How do synergies impact accretion/dilution?”, answer like this:

“Cost synergies usually make a deal more accretive by improving margins and reducing expenses, while revenue synergies add long-term upside. We often calculate break-even synergies to see how much value is needed to make the deal EPS-neutral.”

How to discuss synergies in interviews

In investment banking and private equity interviews, synergy questions come up frequently — because they test how well you can connect strategic thinking with financial modeling.

Your goal isn’t to sound overly technical or memorize definitions — it’s to show that you understand the logic behind how value is created in M&A.

Here’s how to structure a perfect answer:

1. Start with the definition

“Synergies are the additional value created when two companies merge, making the combined entity worth more than the sum of its parts.”

You can optionally add the formula for context:

Synergies = Combined Value − (Value of Buyer + Value of Seller)

2. Differentiate between revenue and cost synergies

“There are two main types: revenue synergies: new sales opportunities through cross-selling or market expansion, and cost synergies, which come from efficiency gains like headcount reduction or procurement savings.”

Keep examples simple and industry-relevant (e.g., “Amazon–Whole Foods” for revenue, “Kraft–Heinz” for cost).

3. Mention realism and risks

“In practice, cost synergies are easier to achieve and often realized within 12–24 months. Revenue synergies take longer and depend on customer behavior and integration success.”

Mention overestimation risks, cultural differences, slow execution, and integration costs, to sound analytical and realistic.

4. Connect to financial impact

“Synergies directly affect valuation and accretion/dilution analysis. Cost synergies usually improve EPS immediately, while revenue synergies drive longer-term value creation.”

If possible, briefly mention “break-even synergies” — the level of value required to make the deal EPS-neutral.

5. End with a balanced summary

“Overall, synergies can transform a deal’s economics — but only if they’re achievable, measurable, and integrated into the financial model with conservative assumptions.”

This framework keeps your answer structured, complete, and natural — exactly what interviewers look for.

Conclusion

Synergies are the core logic behind most M&A transactions. They explain why companies merge, how value is created, and where financial upside comes from. But they’re also one of the biggest risks — because overestimating them can turn an exciting deal into a costly mistake.

In interviews, mastering synergies shows that you understand both the strategic “why” and the financial “how” behind deals. It’s not enough to say that synergies exist — you need to explain their source, timing, and financial impact.

A strong candidate:

- Defines synergies clearly and distinguishes between revenue and cost.

- Explains how to model them in valuation or accretion/dilution analysis.

- Mentions risks and realism, showing awareness of deal execution challenges.

In short, the best M&A professionals, and interview candidates, approach synergies as both an opportunity and a responsibility. They know that real value creation happens not in the spreadsheet, but in successful post-merger integration.

Ready to take the next step toward your investment banking career?

Learn directly from industry professionals with The Thinksters Investment Banking Course — a step-by-step program that helps you master technical skills, interview prep, and real deal analysis.

If you’re preparing for investment banking recruiting, don’t miss How to Write Effective Investment Banking Cover Letters — it walks you through exactly how to craft a compelling story that gets you noticed by top-tier banks.